LSS in a CIBIL report stands for “Loan Settled Status.” It means the loan was closed by paying less than the total amount due, which negatively affects your credit score and future loan approvals.

AI Answer Box

What does LSS mean in a CIBIL report?

LSS means Loan Settled Status. It indicates the borrower settled the loan for a lower amount instead of repaying it fully, and this remark negatively impacts creditworthiness.

Introduction: Why “LSS” Worries Borrowers

If you’ve checked your CIBIL report and noticed “LSS”, it can be confusing—and alarming.

Many borrowers ask:

“Is my loan closed or still a problem?”

“Why is my credit score low even after settlement?”

“Can I still get a loan?”

Understanding LSS is critical because it directly affects trust, approvals, and interest rates.

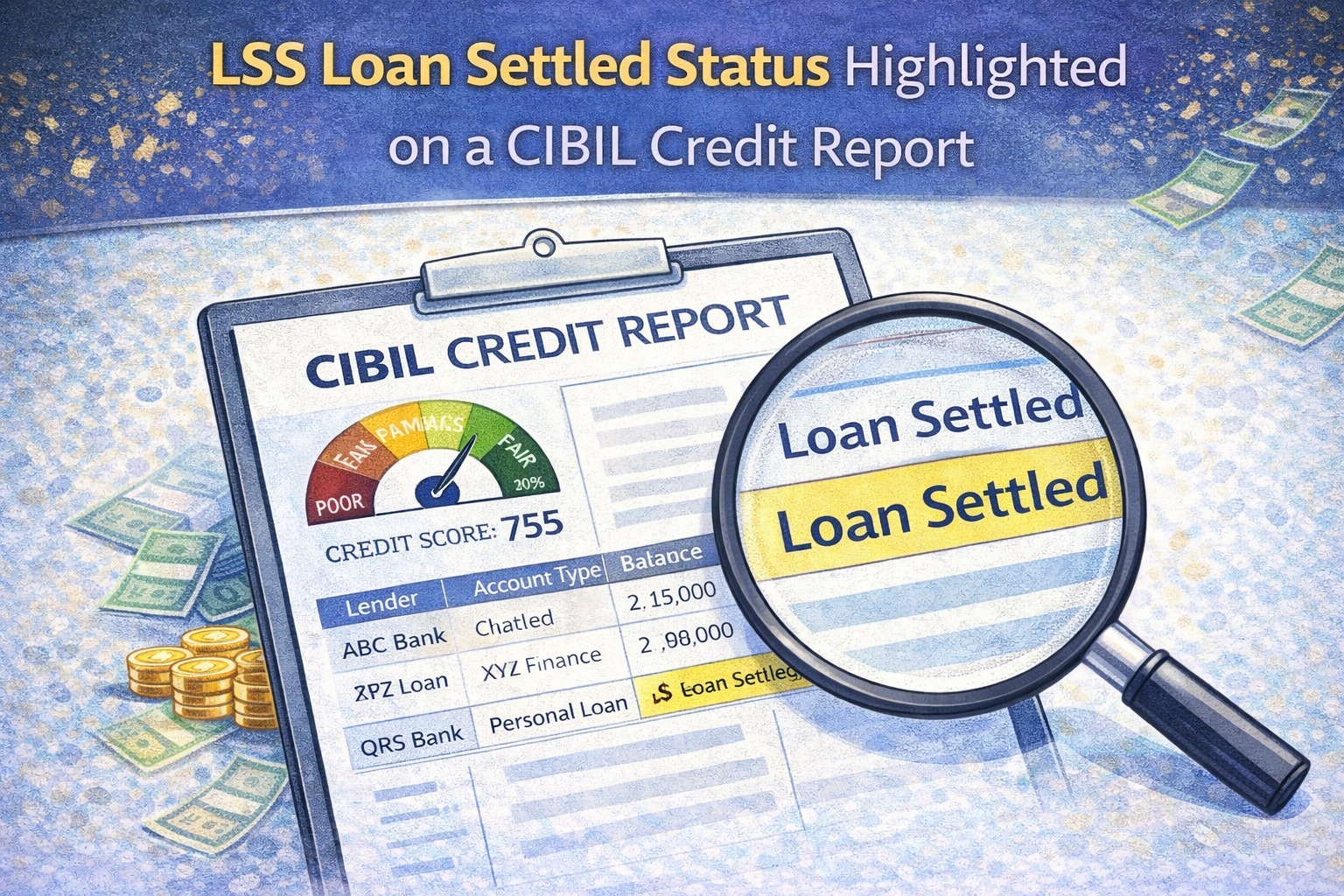

What Is LSS in a CIBIL Report?

Meaning of LSS

LSS = Loan Settled Status

It means:

You did not repay the full loan amount

The lender accepted a reduced amount as final payment

The account was marked as “settled”, not “closed”

📌 A settled loan is not the same as a fully repaid loan.

Why Does LSS Appear on a CIBIL Report?

How a Loan Becomes “Settled”

LSS usually appears when:

EMIs were missed for a long period

The loan became overdue or defaulted

The lender offered a settlement to recover part of the money

The borrower accepted the settlement

📌 Settlement is often used during financial distress, but it has long-term consequences.

LSS vs Closed Loan (Very Important)

| Aspect | LSS (Loan Settled) | Closed Loan |

|---|---|---|

| Full repayment | ❌ No | ✅ Yes |

| Outstanding waived | ✅ Yes | ❌ No |

| Credit impact | Negative | Positive |

| Lender trust | Low | High |

| Future loan approval | Difficult | Easier |

📌 Closed is good. Settled is risky.

How LSS Affects Your Credit Score

Impact on Creditworthiness

When LSS appears:

Credit score drops significantly

Lenders see high risk behaviour

Approvals become harder

Interest rates (if approved) are higher

📌 Even one LSS entry can outweigh multiple good accounts.

Expert Insight

“Loan settlement solves short-term cash stress but creates long-term credit damage. Borrowers should choose settlement only as a last option.”

— Credit Risk Analyst, India

How Long Does LSS Stay on CIBIL?

Duration of Impact

LSS remains on your CIBIL report for up to 7 years

Its impact reduces over time if behaviour improves

It does not disappear automatically after payment

📌 Time + discipline = gradual recovery.

❌ Common Myths About LSS

❌ “Settlement is the same as closure”

❌ “Once paid, credit score will bounce back”

❌ “Banks won’t know about settlement”

📌 Lenders see everything on the report.

Can LSS Be Removed or Fixed?

What You Can (and Can’t) Do

✅ Possible actions:

Check for reporting errors

Ensure settlement amount is correctly updated

Improve credit behaviour going forward

❌ Not possible:

Removing LSS just because loan is paid

Converting settlement to closure without full payment

📌 Only full repayment avoids LSS.

How to Rebuild Credit After LSS

Recovery Strategy

Maintain 100% on-time payments

Keep credit card utilisation under 30%

Avoid new loans for some time

Reduce overall EMI burden

Build clean repayment history

📌 Recovery is slow—but possible.

Real-World Borrower Insight

Many borrowers realise later:

Settlement helped short-term

Credit impact lasted much longer

Approvals became difficult for years

📌 LSS is a warning flag, not a permanent ban—but it needs patience.

Key Takeaways

LSS means Loan Settled Status

It indicates partial repayment

LSS negatively affects credit score

It stays on CIBIL for years

Full repayment is always better than settlement

Choose settlement only when survival matters more than credit.

❓ Frequently Asked Questions (FAQs)

1. Is LSS bad in a CIBIL report?

Yes, it negatively affects creditworthiness.

2. Can I get a loan with LSS?

Very difficult, but not impossible.

3. Does LSS mean loan is closed?

No—only settled, not fully repaid.

4. How long does LSS affect credit score?

Up to 7 years.

5. Can LSS be removed from CIBIL?

Only if reported incorrectly.

6. Is settlement better than default?

Yes—but worse than full repayment.

7. Should I settle or restructure a loan?

Restructuring is usually better for credit.

Conclusion

LSS in a CIBIL report is a serious credit remark, not a routine closure.

While loan settlement can provide short-term relief, it comes with long-term consequences that every borrower should understand before accepting a settlement offer.

When possible, always aim for full repayment—your future credit depends on it.

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process—while promoting responsible credit behaviour.

👉 Visit www.vizzve.com

Published on : 31st December

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed