Banks are rejecting self-employed loan applications due to inconsistent income patterns, poor credit history, insufficient documentation, high business risk, and flagged account behavior — all of which raise underwriting concerns in 2026.

AI Answer Box

Self-employed borrowers often face loan rejections because lenders worry about unstable cash flows, weak documentation, insufficient credit history, high existing obligations, and unpredictable business performance. Strengthening records and demonstrating consistency can improve approval rates.

Why Self-Employed Loans Are Harder to Get Approved Now

Unlike salaried employees with fixed monthly salaries, self-employed borrowers often show:

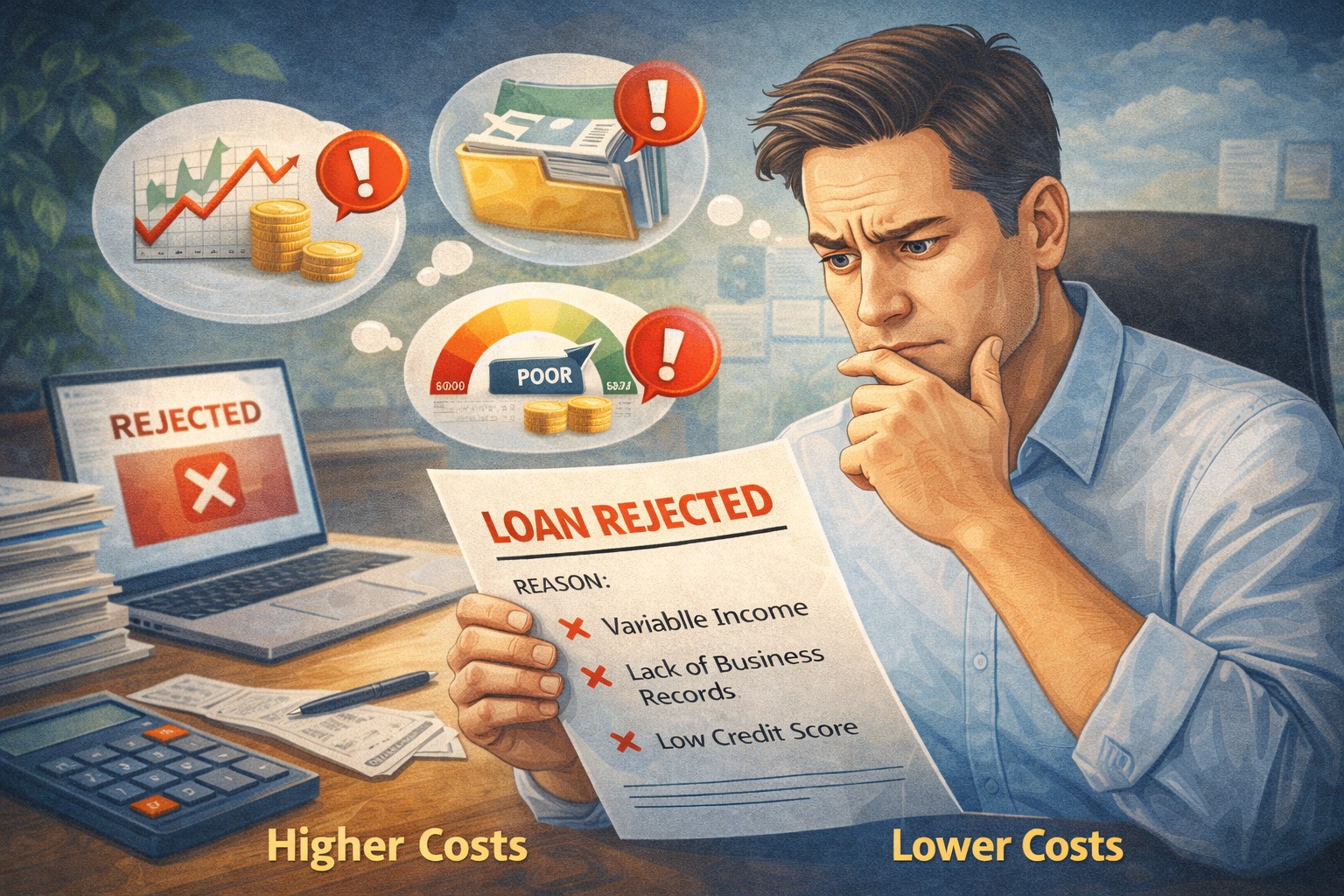

Variable monthly income

Seasonal fluctuations

Cash transactions not reflected in bank statements

Multiple credit sources

Banks see this as higher risk — and in a cautious credit environment, risk leads to more rejections.

What Banks Analyze Before Approving Loans

Before approving a loan, banks typically evaluate:

| Factor | What Lenders Worry About |

|---|---|

| Income Stability | Variable or inconsistent revenue |

| Documentation | Missing GST, ITR, or incomplete records |

| Credit Score | Low or thin credit history |

| Cash Flow Patterns | Unpredictable inflows/outflows |

| Existing Debts | High liability vs income |

| Business Viability | Market, demand, and future revenue risk |

| Banking Behavior | Frequent overdrafts, low balances |

Self-employed borrowers often score lower on these metrics compared to salaried counterparts.

Key Reasons Banks Are Rejecting Self-Employed Loans

1️⃣ Fluctuating Monthly Income

Self-employment rarely guarantees fixed monthly income. Even if annual income looks strong, month-to-month variability raises red flags.

Banks rely on consistent inflow trends to estimate EMI capacity.

2️⃣ Weak or Incomplete Documentation

Lenders want:

Verified ITRs (2–3 years consistently)

GST returns

Bank statements showing business revenue

Proof of business existence (licenses, contracts)

Missing or patchy documents often trigger automatic rejections.

3️⃣ Thin or Poor Credit History

Even if income is good, a thin credit profile or previous delinquencies can derail approvals.

Lenders look for:

Timely past payments

Low credit utilization

Healthy credit mix

Inconsistent repayment signals higher repayment risk.

4️⃣ Unpredictable Cash Flow Patterns

Cash flow is critical — especially for self-employed loans.

Banks analyze:

Peaks and troughs in bank statement balance

Large withdrawals without explanation

Seasonal receipts

Large personal usage from business accounts

Stable cash flow means higher confidence.

5️⃣ High Existing Liabilities

Banks calculate Debt-to-Income (DTI) ratios.

High existing EMIs from:

Personal loans

Business loans

Credit cards

can reduce borrowing capacity significantly.

6️⃣ Industry or Market Risk Flags

Some sectors are riskier (seasonal businesses, high volatility).

Lenders may reject or offer:

Higher interest rates

Lower loan amounts

Additional security

Self-Employed vs Salaried: Lender Perspective

| Criteria | Salaried | Self-Employed |

|---|---|---|

| Income predictability | High | Moderate–Low |

| Documentation uniformity | Standard | Variable |

| Credit scoring reliability | Strong | Often weak |

| Cash flow clarity | Clear | Often unclear |

| Underwriting confidence | High | Lower |

This gap explains why self-employed loans face more scrutiny.

Expert Insight

“For underwriting, the biggest concern with self-employed borrowers is consistency and predictability. Without clear patterns in income and cash flow, lenders assign a higher risk score, which leads to tighter conditions or outright rejections.”

— Retail & SME Credit Specialist

How Self-Employed Borrowers Can Improve Approval Chances

📌 1. Maintain Consistent Documentation

File ITRs for at least 2–3 years

Keep business receipts, GST, and invoices well-organized

📌 2. Show Stable Bank Balances

Aim for:

Regular cash flow

Avoid frequent overdrafts

Keep balance patterns clean

📌 3. Improve Credit Score

Work on:

Paying EMIs and cards on time

Reducing credit utilization

Keeping credit history healthy

📌 4. Reduce Existing Liabilities

Pay down:

High-interest debts

Credit card balances

This improves DTI and shows repayment discipline.

📌 5. Provide Collateral When Possible

Secured loans reduce risk and can improve approval odds.

Borrower Checklist for Self-Employed Loan Success

| Action | Why It Helps |

|---|---|

| File 3 years of ITR | Shows income consistency |

| Update GST returns | Verifies business activity |

| Clean bank statements | Demonstrates cash flow |

| Improve credit score | Signals repayment discipline |

| Reduce DTI ratio | Enhances capacity |

| Provide business proof | Reduces risk perception |

Key Takeaways

Self-employed loans are more complex due to variable income patterns.

Banks focus on cash flow, documentation, and credit behavior.

Strong credit habits and complete paperwork boost approval chances.

Preparatory planning beats repeated applications.

Conclusion

Self-employed loan rejections aren’t about “penalizing” entrepreneurship — they’re about risk assessment. When income is unpredictable, documentation incomplete, or credit behavior inconsistent, lenders tighten credit decisions. Self-employed borrowers who prioritize consistency, transparency, and preparation stand the best chance of approval in 2026.

❓ Frequently Asked Questions (FAQs)

1. Why do banks reject self-employed loan applications more often?

Banks worry about variable income, poor documentation, and cash flow ambiguity, all of which increase risk.

2. Can I improve approval chances quickly?

Yes — by organizing documents, clearing high debt, and correcting credit behavior over 3–6 months.

3. How many years of ITR do banks typically want?

Most lenders prefer 2–3 years of consistent ITRs.

4. Does credit score matter for self-employed loans?

Yes — a strong credit score demonstrates repayment discipline.

5. Will a guarantor help?

Yes — a guarantor or collateral increases approval probability.

6. Do banks favor salaried borrowers over self-employed?

Generally yes, because salaried income is more predictable.

7. Do digital lenders have different standards?

Digital lenders rely on automated risk models, but still weigh income consistency and credit history heavily.

8. Does GST registration help?

Yes — it proves business legitimacy and revenue tracking.

9. Can seasonal income hurt my chances?

Yes — unpredictable or seasonal inflows make underwriting cautious.

10. Should self-employed borrowers avoid loans?

No — just prepare documentation better and use strategic financial planning.

Published on : 16th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed