Selling a property often results in high capital gains tax, especially if the property has appreciated significantly over the years. To reduce this tax burden, the government allows individuals to claim exemptions — most commonly through Section 54 and the Capital Gains Account Scheme (CGAS).

With the new CGAS rules, the process of claiming tax benefits has become more flexible, more transparent, and far more seller-friendly. If you’re planning to sell property, these changes can help you save a substantial amount of tax.

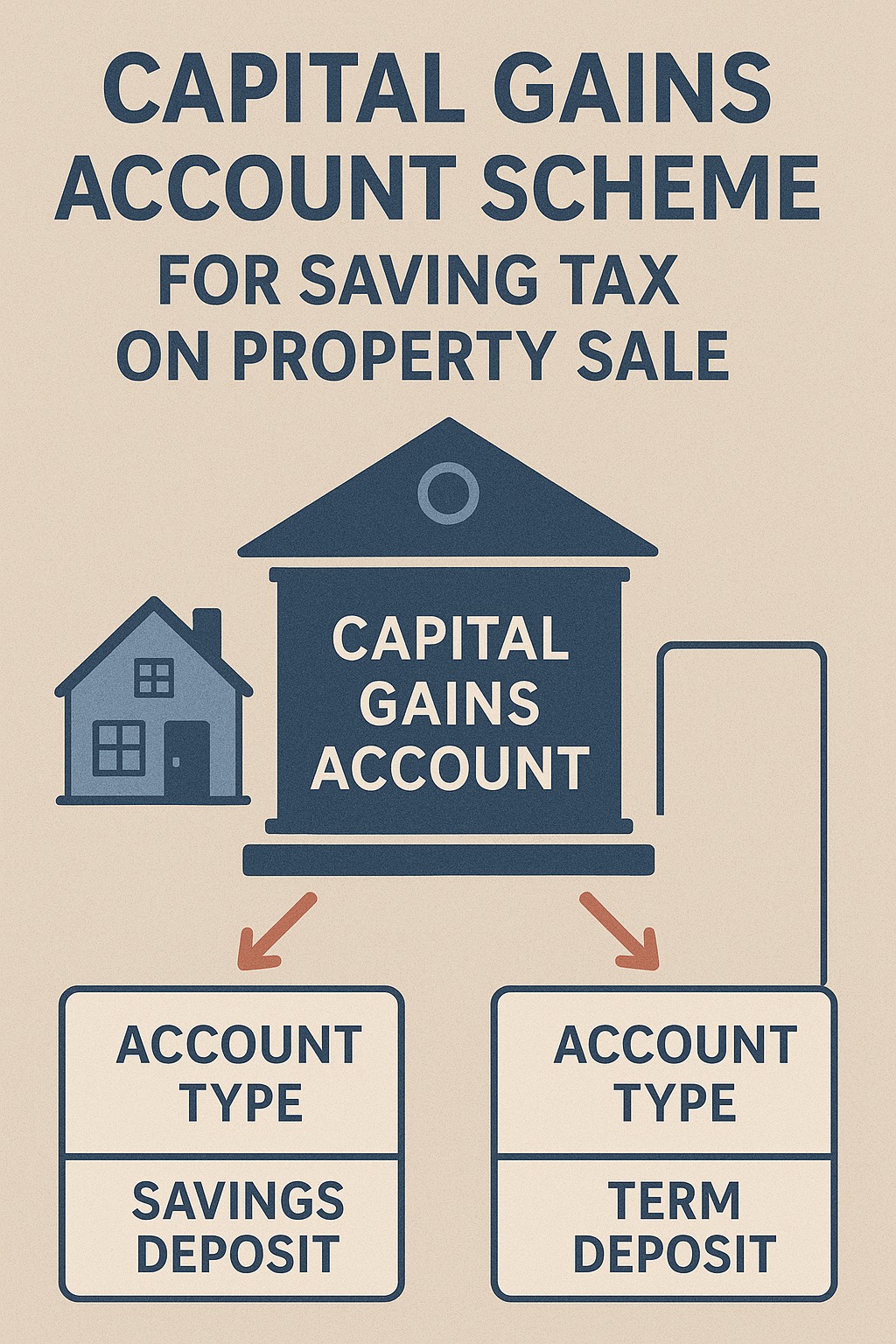

What Is CGAS and Why Does It Matter?

CGAS (Capital Gains Account Scheme) allows property sellers to park their capital gains temporarily if they haven’t yet bought or constructed a new house.

This helps taxpayers claim exemptions under:

Section 54 – reinvest gains from selling a house into a new house

Section 54F – reinvest gains from selling any asset into a new house

Earlier, strict timelines and procedures made many sellers lose out on benefits. The new rules simplify this.

Key Changes in the New CGAS Rules — And How They Help You

1. Extended Flexibility for Withdrawal & Re-Deposit

Previously, taxpayers struggled because withdrawals had rigid rules.

Now, the new system allows:

Easier withdrawal of funds

Re-depositing unused amounts

More transparency in utilisation

👉 Benefit: You can manage construction delays or project changes without losing eligibility.

2. Wider Bank Availability & Faster Processing

Earlier, only a few banks handled CGAS accounts.

Today, more authorised banks and better digital processing mean:

Faster account opening

Faster verification

Easier documentation

👉 Benefit: Reduced hassle and quicker capital gains planning.

3. Greater Clarity on Time Limits

Under Sections 54 and 54F:

2 years to buy a new house

3 years to construct a house

CGAS deposit required before the ITR filing deadline

The new rules highlight these timelines with improved clarity, helping taxpayers avoid errors.

👉 Benefit: Lower chances of losing exemption due to technical mistakes.

4. Better Tracking & Documentation

Modernised rules ensure:

Clear tracking of deposits

Documented withdrawals

Simple proof submission to claim exemption

👉 Benefit: Smooth processing during tax filing and fewer queries from authorities.

5. Protection Against Losing Exemption

Earlier, improper usage or delays could lead to entire tax exemption being reversed.

The new guidelines provide structured compliance, reducing the risk of losing benefits.

👉 Benefit: Higher chances of 100% tax savings on capital gains.

How Much Tax Can You Actually Save?

If you reinvest correctly using CGAS under Section 54/54F, you can save up to 100% of your long-term capital gains tax.

For example:

If you sold property and made ₹40 lakh capital gains, you could save the entire amount by depositing it under CGAS and using it for buying/constructing a house within the permitted time.

Who Should Use CGAS?

People planning to buy a new house after selling old property

Sellers waiting for construction projects to complete

Those dealing with builder delays

Taxpayers who want to avoid high upfront capital gains tax

FAQs

1. What happens if I don’t use the CGAS amount within the allowed time?

The unused amount gets added back to your taxable income.

2. Can I withdraw CGAS funds anytime?

Yes, with bank approval and proper documentation.

3. Do I need to use the entire deposited amount?

No, you can withdraw in parts as per the construction or purchase requirement.

4. Can I deposit the amount after selling property?

Yes, but it must be deposited before the ITR filing deadline to claim exemption.

5. Are the new CGAS rules beneficial?

Absolutely — they offer more flexibility, better processing, and increased taxpayer protection.

Published on : 25th November

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed

Source Credit : MINT