Introduction

India’s lending landscape is changing rapidly in 2026. The fastest-growing segment today is small personal loans under ₹50,000, driven by rising everyday expenses, short-term cash gaps, digital loan apps, and easier access through UPI-based credit products.

These small-ticket loans—once seen only as emergency credit—have now become mainstream borrowing tools. NBFCs report 35–50% YoY growth in this category, and digital lenders say 7 out of 10 loan applications fall under ₹50,000.

But why is this happening?

Let’s break down the hidden factors.

AI ANSWER BOX

Small personal loans under ₹50,000 are rapidly increasing in India due to rising daily expenses, short-term cash shortages, quick approval through digital apps, UPI-based credit lines, and low documentation requirements.

Borrowers choose these loans for convenience, instant disbursal, and flexible repayment, especially during emergencies, online shopping, and monthly lifestyle spending.

Why Short-Term Credit Demand Is Growing in India (2026)

1. Rising Cost of Living

Food, transport, utilities, and education have seen a 10–20% increase in many cities, creating monthly cash shortages.

2. Increase in Gig Workers & Freelancers

India has over 70 million gig workers who face income irregularity — making small loans a buffer.

3. Easy Access Through Digital Loan Apps

Loan apps offer:

5-minute approval

Minimal KYC

No bank visits

No paperwork

Perfect for short-term credit.

4. UPI Credit Line Launch

UPI-based credit lets borrowers access ₹5,000–₹50,000 instantly via QR codes or UPI apps.

5. Emergency Medical & Personal Expenses

Small-ticket loans are widely used for:

Medicines

Doctor visits

Utility bills

Travel emergencies

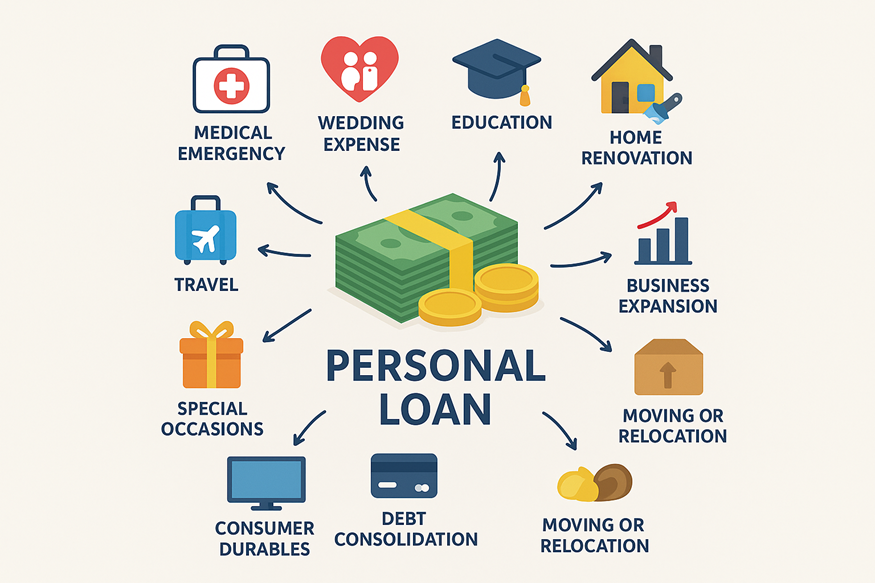

What People Use Small Loans Under ₹50,000 For

| Usage Category | Share (2026) |

|---|---|

| Medical emergencies | 28% |

| Online shopping | 21% |

| Bill payments | 16% |

| Travel & fuel | 14% |

| Education fees | 10% |

| Home repairs | 11% |

Small Personal Loans Vs Large Personal Loans — What’s the Difference?

| Feature | Small Loans (<₹50,000) | Regular Personal Loans |

|---|---|---|

| Approval | Instant | 4–48 hours |

| Docs needed | Minimal | Full KYC + bank statements |

| Interest rate | Higher | Lower |

| Tenure | 1–12 months | 1–5 years |

| Purpose | Daily expenses | Major expenses |

| Ideal for | Students, salaried, gig workers | Salaried borrowers |

Why Banks & NBFCs Are Pushing Small Loans

1. Higher Profit Margins

Interest rates on small loans are 18–36%, much higher than big loans.

2. Low Acquisition Costs

Fintech apps automate KYC, reducing staff and branch expenses.

3. Safe Borrower Base

Most small-loan borrowers repay quickly to maintain eligibility.

4. Higher Repeat Borrowing

Borrowers often take 4–6 small loans annually.

Risks Small Borrowers Should Understand

| Risk | Impact |

|---|---|

| High interest rates | EMI burden increases |

| App fraud | Unregulated lenders cheat users |

| Debt cycle | Repeat loans lead to dependency |

| Hidden fees | Processing charges + GST |

Small Loan Interest Rate Trends in 2026

| Lender Type | Avg Interest | Notes |

|---|---|---|

| Banks | 12–18% | Lower but stricter checks |

| NBFCs | 18–30% | Fast approvals |

| Loan Apps | 24–36% | High APR, short tenure |

| UPI Credit Line | 12–22% | Cheapest for small borrowers |

Expert Commentary

Small-ticket credit is becoming the backbone of India’s digital economy. As incomes fluctuate and expenses rise, borrowers are relying on micro credit rather than large loans.

This shift is not entirely bad — but borrowers must avoid relying on apps with hidden fees and should prioritize regulated lenders.

UPI credit line will disrupt small personal loans significantly by offering lower APR and minimal processing fees.

Key Takeaways

Small personal loans under ₹50,000 are booming in India

UPI Credit Line is accelerating small-ticket borrowing

Gig workers and young professionals are driving the demand

Small loans are quick but come with higher interest rates

Borrowers must avoid illegal lending apps

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and easy approval.

👉 Apply instantly at www.vizzve.com

FAQs

1. Why are Indians taking more short-term loans?

Due to rising expenses and instant access.

2. What is the typical small loan amount?

₹10,000–₹50,000.

3. Are small loans more expensive?

Yes, interest rates are higher.

4. Which is cheaper—UPI Credit or small personal loan?

UPI Credit Line is usually cheaper.

5. Who takes the most small loans?

Young professionals, gig workers, students.

6. Do small loans affect credit score?

Yes, missed payments reduce the score.

7. How fast is approval?

Instant through apps.

8. Is KYC required?

Yes, basic KYC.

9. Are NBFC small loans safe?

Yes, if RBI regulated.

10. Are loan apps risky?

Unregulated apps = dangerous.

11. Tenure for small loans?

1–12 months.

12. Any hidden charges?

Processing fee + GST.

13. Can I get ₹50,000 without salary slip?

Possible through NBFCs.

14. What is the biggest problem?

Debt cycle from repeat borrowing.

15. Best alternative to small loans?

UPI Credit Line or salary advance.

Published on : 8th December

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed