Most credit damage doesn’t happen because of big financial failures.

It happens because of small, short-term decisions that feel harmless in the moment.

Paying the minimum due.

Taking a quick loan.

Overspending “just this once.”

These decisions solve today’s problem—but quietly harm your credit health for years.

Let’s understand how short-term financial choices damage long-term credit health, and how to avoid these traps in 2026.

AI Answer Box

Short-term financial decisions like impulse borrowing, high credit card usage, minimum payments, and frequent loan enquiries can hurt long-term credit health. Credit scores reward consistency and discipline, not quick fixes, making early mistakes costly over time.

Quick Summary Box

Credit scores track patterns, not moments

Short-term relief often creates long-term damage

Credit cards and EMIs have lasting impact

Recovery takes months or years

Discipline beats quick fixes

Why Credit Health Is a Long-Term Game

Credit scores are designed to answer one question:

👉 “How risky will this borrower be in the future?”

That’s why credit systems:

Track behaviour over time

Penalise repeated short-term fixes

Reward stability and patience

A single impulsive choice may seem small—but patterns form quickly.

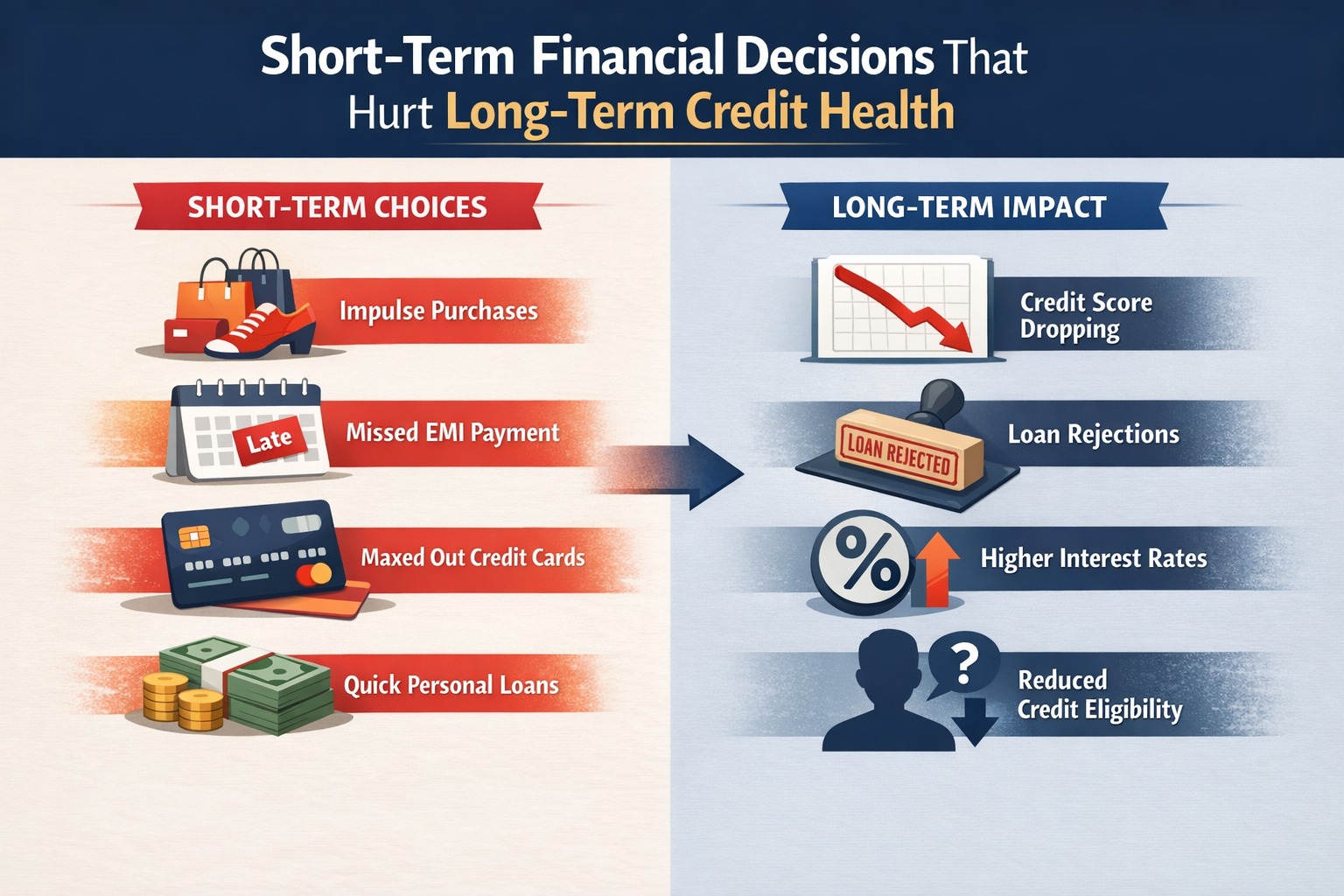

Short-Term Decisions That Damage Long-Term Credit Health

1. Paying Only the Minimum Credit Card Due

It feels safe—but it’s not.

Short-term benefit:

Avoids late payment

Long-term damage:

High interest accumulation

Credit utilisation stays high

Score weakens slowly

This is one of the most common silent credit killers.

2. Using Full Credit Card Limit “Temporarily”

Even short-term high usage sends a risk signal.

Why lenders worry:

Signals cash flow stress

Indicates dependency on credit

Even if you repay later, the score impact happens immediately.

3. Taking Quick Loans for Small Needs

Instant loans feel convenient—but:

Hidden long-term costs:

Frequent enquiries

Short credit cycles

Overlapping EMIs

Multiple small loans create a high-risk borrowing pattern.

4. Skipping EMIs Once to “Manage Cash”

Missing one EMI feels manageable.

Reality:

Late payments stay on reports for years

One delay can undo months of discipline

Credit systems do not forget quickly.

5. Closing Credit Accounts to “Simplify Finances”

This feels responsible—but can backfire.

Why closing hurts:

Shortens credit history

Raises utilisation ratio

Reduces credit depth

Old accounts actually support long-term credit health.

Short-Term Relief vs Long-Term Credit Impact

| Decision | Feels Helpful Now | Long-Term Credit Impact |

|---|---|---|

| Minimum card payment | Yes | Negative |

| Full credit limit usage | Yes | Negative |

| Multiple small loans | Yes | Negative |

| EMI delay | Yes | Strong negative |

| Closing old accounts | Yes | Negative |

Why Credit Recovery Takes So Long

Short-term damage heals slowly because:

Negative marks stay for years

Trust rebuilds gradually

Lenders prioritise recent behaviour

One bad month can take six good months to repair.

How to Protect Long-Term Credit Health

Smart Long-Term Credit Habits:

Pay credit cards in full

Keep usage below 30%

Avoid impulse loans

Never skip EMIs

Keep old accounts active

Plan borrowing, don’t react

Long-Term Credit Health Checklist

| Area | Safe Practice |

|---|---|

| EMI payments | On time, always |

| Card utilisation | Below 30% |

| Loan frequency | Minimal |

| Old accounts | Keep active |

| Credit review | Quarterly |

Expert Commentary: Credit Scores Punish Shortcuts

“Credit scoring models are built to detect shortcuts. What feels like a temporary solution often looks like a long-term risk.”

— Credit Risk Analyst

Key Takeaways

Credit health is built slowly, damaged quickly

Short-term relief often causes long-term harm

Credit cards influence scores more than people think

Discipline beats convenience

Long-term thinking protects financial freedom

❓ Frequently Asked Questions (FAQs)

1. Can one short-term mistake hurt my credit score?

Yes, even one mistake can impact your score for months.

2. Is paying minimum due harmful?

Yes, it keeps utilisation high and weakens credit health.

3. Do small loans affect credit score?

Yes, frequent small loans increase risk perception.

4. How long does credit damage last?

Minor damage may recover in 3–6 months; serious issues can last years.

5. Is closing unused cards good?

Not always—older cards often help your credit profile.

6. Does high spending matter if I repay later?

Yes, utilisation affects score immediately.

7. How often should I review my credit?

At least once every quarter.

8. What’s the safest credit habit?

Never miss payments and keep borrowing planned.

Conclusion: Think Long-Term, Even When Decisions Feel Small

Credit health isn’t destroyed by disasters—it’s damaged by decisions made in a hurry.

Every short-term choice trains your credit profile to look safe or risky.

In 2026, the smartest borrowers don’t ask, “Will this help me today?”

They ask, “How will this look six months from now?”

📌 Short-term thinking costs long-term freedom. Discipline protect it.

Published on : 1st January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed