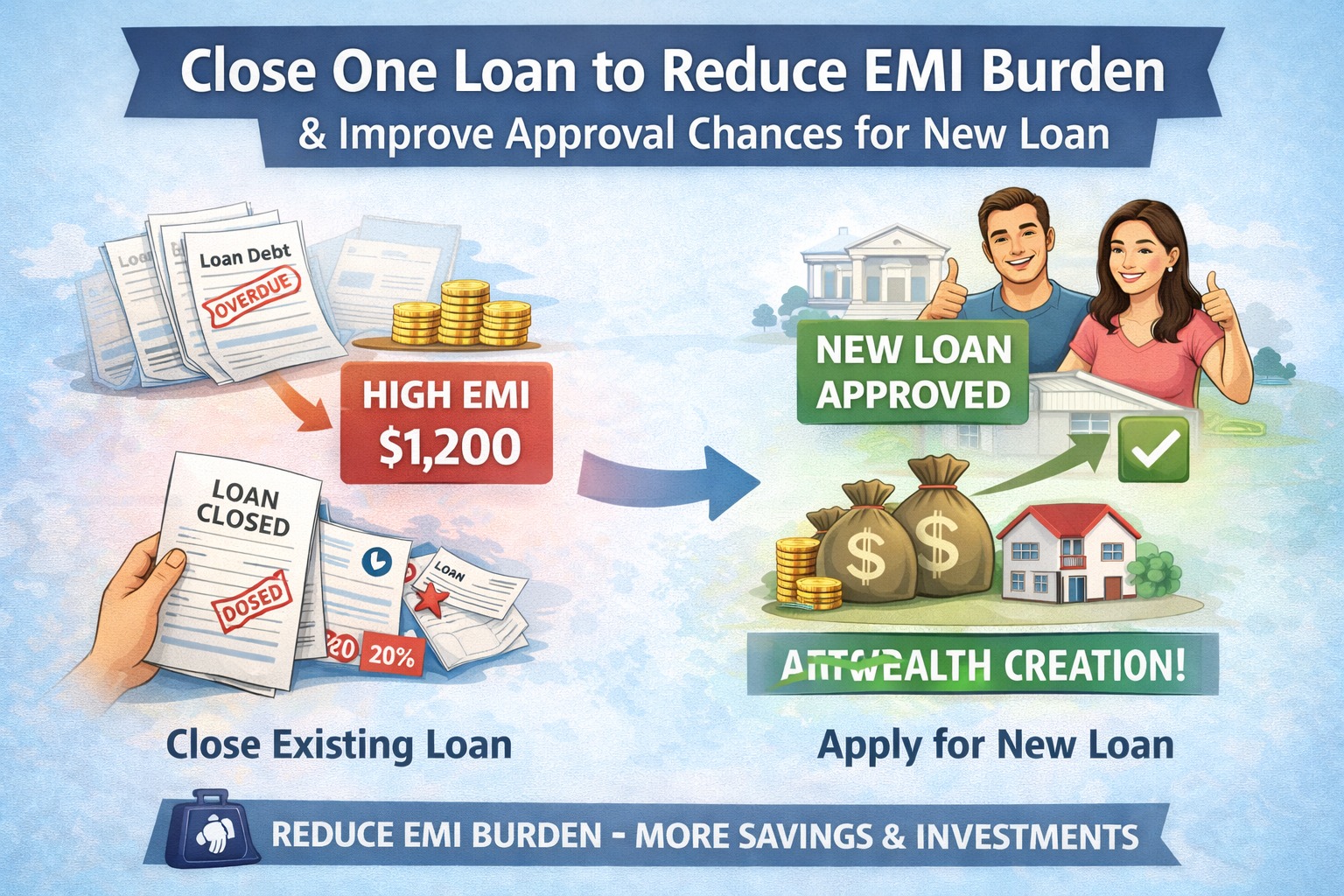

Closing an existing loan improves approval for another by freeing EMI capacity, strengthening credit behaviour, and reducing lender risk perception.

AI Answer Box

Does closing a loan improve chances of getting another loan?

Yes. Closing a loan lowers your EMI burden, improves cash-flow ratios, and signals disciplined repayment—making lenders more confident in approving your next loan.

Introduction: Why Borrowers Get Rejected Despite “Good Income”

One of the most confusing moments for borrowers is this:

“My income is higher now, but my loan still got rejected.”

Often, the issue isn’t income.

It’s existing loans.

In modern lending, approvals are less about how much you earn and more about how much you’re already committed to paying.

That’s why closing one loan can dramatically improve approval for another.

Expert Commentary

“Lenders look at repayment capacity, not just earnings. Reducing existing obligations is one of the fastest ways to improve loan eligibility.”

— Credit Underwriting Specialist, India

How Lenders Actually Decide Loan Approval

It’s About Risk, Not Reward

When you apply for a loan, lenders evaluate:

Existing EMIs

Credit score

Repayment history

Stability and consistency

Debt-to-income ratio

📌 Every active loan increases perceived risk, even if you’ve never missed a payment.

Reason #1: Closing a Loan Frees EMI Capacity

EMI Capacity Is a Hard Limit

Most lenders prefer:

Total EMIs ≤ 30–35% of monthly income

When one loan closes:

Monthly obligations drop

Free cash flow increases

Eligibility instantly improves

📌 This single change can turn a rejection into an approval.

Example: EMI Capacity in Action

| Scenario | Monthly Income | Existing EMI | EMI Ratio |

|---|---|---|---|

| Before loan closure | ₹60,000 | ₹22,000 | 36% ❌ |

| After closing loan | ₹60,000 | ₹15,000 | 25% ✅ |

📌 Same income. Same person. Very different outcome.

Reason #2: Lower Risk Perception for Lenders

Fewer Loans = Cleaner Profile

Multiple active loans signal:

Dependency on credit

Higher stress risk

Potential over-borrowing

Closing one loan shows:

Discipline

Ability to complete commitments

Controlled borrowing behaviour

📌 Lenders reward completion, not just activity.

Reason #3: Credit Score Responds Positively (Over Time)

Closing a loan can:

Improve credit mix

Reduce utilisation pressure

Strengthen repayment history

⚠️ Important:

Score improvement is gradual, not instant

The real benefit is eligibility, not just score points

Reason #4: Psychological Confidence Improves Decisions

Borrowers with fewer loans:

Choose better tenure

Avoid emotional borrowing

Negotiate better terms

Plan repayments realistically

📌 Better decisions lead to better approvals.

Real-World Experience Insight

Many borrowers notice:

Loan rejections disappear after one closure

Lower interest offers become available

Approval timelines shorten

This happens even when:

Income hasn’t changed

Credit score moves only slightly

📌 The system values lower load, not just higher score.

Which Loan Should You Close First?

Smart Loan-Closing Strategy

✅ Priority Order:

High-interest personal loans

Small loans with high EMI impact

Loans nearing completion

📌 Closing even a small loan can free meaningful EMI space.

Should You Close a Loan Early Just to Take Another?

Only If It Improves Net Position

Closing a loan makes sense if:

It reduces EMI stress

It improves approval odds

It lowers long-term cost

It doesn’t make sense if:

It drains emergency funds

It creates short-term pressure

📌 Always improve overall flexibility, not just eligibility.

A Simple Borrowing Rule

The fewer loans you carry, the more options you unlock.

Approval power comes from:

Completion

Capacity

Consistency

Key Takeaways

Loan approvals depend on EMI load, not just income

Closing one loan frees capacity instantly

Lenders prefer fewer, completed loans

Credit behaviour matters more than credit appetite

Strategic loan closure improves financial leverage

Sometimes, the fastest way to get a new loan is to finish an old one.

❓ Frequently Asked Questions (FAQs)

1. Does closing a loan improve credit score immediately?

Not immediately, but it improves profile quality.

2. Which loan should I close first?

High-interest or high-EMI loans.

3. Can closing a small loan help approval?

Yes, if it improves EMI ratio.

4. Will lenders see closed loans positively?

Yes—completion signals discipline.

5. Is it bad to have multiple loans?

Not bad, but it reduces eligibility.

6. Does prepayment help loan approval?

Yes, by freeing EMI capacity.

7. Should I close a loan using savings?

Only if emergency needs are protected.

8. Will interest rate improve after closing a loan?

Often yes, due to lower risk.

9. Does credit score matter more than EMI ratio?

Both matter—but EMI ratio is decisive.

10. How soon can I apply after closing a loan?

Usually after credit records update (1–2 months).

Conclusion

Loan approval isn’t about adding more credit—it’s about managing what you already have.

Closing one loan:

Reduces stress

Improves eligibility

Strengthens credibility

Sometimes, less debt is the fastest path to more access.

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process.

👉 Apply now at www.vizzve.com

Published on : 30th December

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed