Introduction

Every loan follows a defined lifecycle—whether it’s a personal loan, home loan, or business loan.

From the moment you apply to the day you receive a loan closure certificate, banks track each stage carefully. Understanding this lifecycle helps borrowers avoid mistakes, reduce costs, and protect credit scores.

This guide explains the entire loan journey step by step, in simple language.

AI Answer Box

Short Answer:

The lifecycle of a loan includes application, credit assessment, approval, disbursement, EMI repayment, and final closure, with borrower behaviour at each stage affecting cost and credit health.

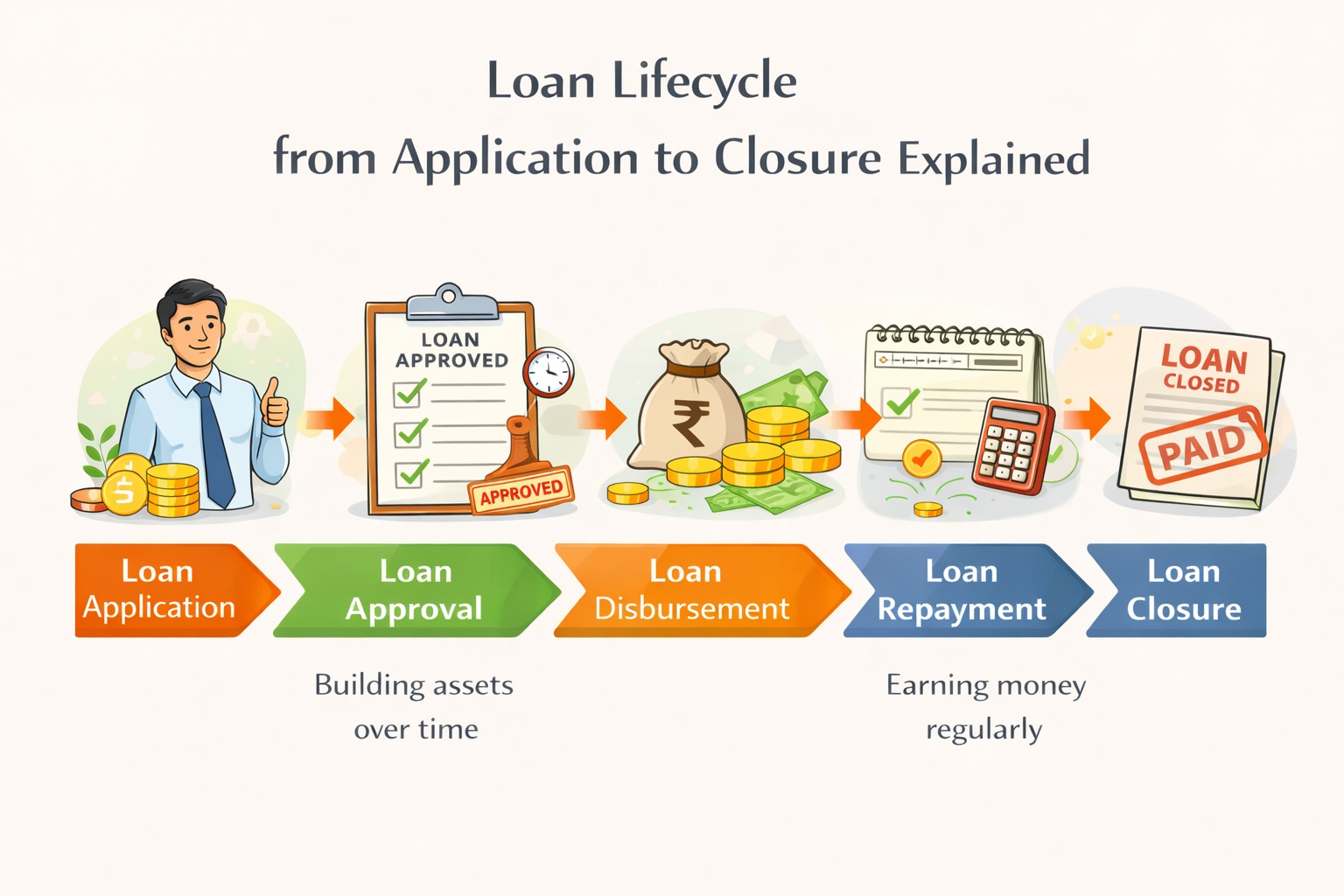

Stage 1: Loan Application

This is where the journey begins.

What Borrowers Do

Choose loan type and amount

Submit KYC, income, and bank details

Authorise credit bureau checks

What Banks Check

Credit score & repayment history

Income stability

Existing EMIs

📌 Mistake here = delays or rejection.

Stage 2: Credit Assessment & Underwriting

Banks now focus on credit quality, not just approval.

They assess:

EMI-to-income ratio

Cash-flow sustainability

Employment or business stability

Under guidelines of the Reserve Bank of India, lenders apply stress testing before approval.

Stage 3: Loan Approval & Sanction

If approved, you receive a sanction letter detailing:

Approved loan amount

Interest rate

Tenure

EMI amount

Fees and conditions

📌 Approval ≠ disbursement yet.

Stage 4: Documentation & Agreement Signing

Borrowers must:

Sign loan agreement

Accept repayment schedule

Provide collateral (if applicable)

At this stage, terms become legally binding.

Stage 5: Loan Disbursement

After documentation:

Funds are credited to your account

Or paid directly to seller/builder

📌 Interest usually starts from disbursement date.

Stage 6: EMI Repayment Phase

This is the longest and most critical stage.

What Happens Monthly

EMI auto-debit

Interest + principal adjustment

Credit bureau updates

Why Discipline Matters

Missed EMIs hurt credit score

Penalties increase cost

Repeated delays trigger risk flags

Stage 7: Mid-Cycle Events (Optional but Common)

During the loan tenure, borrowers may:

Prepay part of the loan

Refinance at lower rates

Restructure EMIs during stress

Each action affects:

Total interest paid

Loan tenure

Future loan eligibility

Loan Lifecycle Snapshot

| Stage | Borrower Impact |

|---|---|

| Application | Eligibility & approval |

| Assessment | Loan amount decision |

| Disbursement | Interest start |

| Repayment | Credit score impact |

| Prepayment | Cost reduction |

| Closure | Credit health reset |

Stage 8: Loan Closure

Once final EMI is paid:

Loan account is closed

No further interest accrues

Borrower Must Collect:

Loan closure letter

No-dues certificate

Collateral release (if any)

📌 This step is often ignored—but critical.

Stage 9: Post-Closure Credit Update

After closure:

Lender updates credit bureaus

Loan status marked “closed”

This improves:

Credit utilisation

Future loan eligibility

Common Mistakes Across the Loan Lifecycle

Applying without checking EMI affordability

Ignoring sanction letter terms

Missing auto-debit setup

Delaying closure documentation

Forgetting to check credit report after closure

Real-World Lending Insight

From borrower case reviews, many credit issues arise after approval, not before. Most long-term damage happens during repayment and closure stages, not application.

How to Manage a Loan Smartly

Borrow below maximum eligibility

Keep EMIs under 35% of income

Set auto-debit reminders

Prepay whenever surplus allows

Close loan cleanly and document it

Loan Lifecycle vs Credit Score Impact

| Stage | Credit Impact |

|---|---|

| Application | Minor enquiry hit |

| Approval | Neutral |

| On-time EMIs | Positive |

| Missed EMIs | Negative |

| Closure | Positive |

Key Takeaways

A loan is a journey, not a transaction

Repayment behaviour matters most

Prepayment reduces cost

Closure documentation is essential

Understanding the lifecycle protects credit

Frequently Asked Questions

1. What is the lifecycle of a loan?

From application to final closure.

2. When does interest start?

From disbursement date.

3. Does loan approval affect credit score?

Only slightly via enquiry.

4. Which stage affects credit score most?

EMI repayment stage.

5. Can loans be prepaid?

Yes, subject to terms.

6. Is foreclosure same as closure?

Yes, after full repayment.

7. Do missed EMIs affect future loans?

Yes, significantly.

8. Should I keep closure documents?

Absolutely.

9. Does loan closure improve credit score?

Yes, over time.

10. Are all loans same lifecycle?

Yes, structure is similar.

11. Is refinancing part of lifecycle?

Yes, as a mid-cycle event.

12. What’s the biggest borrower mistake?

Ignoring post-closure updates.

Conclusion: Borrow Smart, Finish Strong

A loan doesn’t end with approval—it ends with proper closure.

Borrowers who understand the full loan lifecycle save money, avoid stress, and protect their financial future. Smart borrowing isn’t just about getting a loan—it’s about managing it end to end.

CTA: Smarter Borrowing Support

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process. Apply at www.vizzve.com.

Published on : 24th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed