When it comes to your credit score, most people focus on timely repayments or credit utilization. But there’s another lesser-known factor that plays a big role — your credit mix.

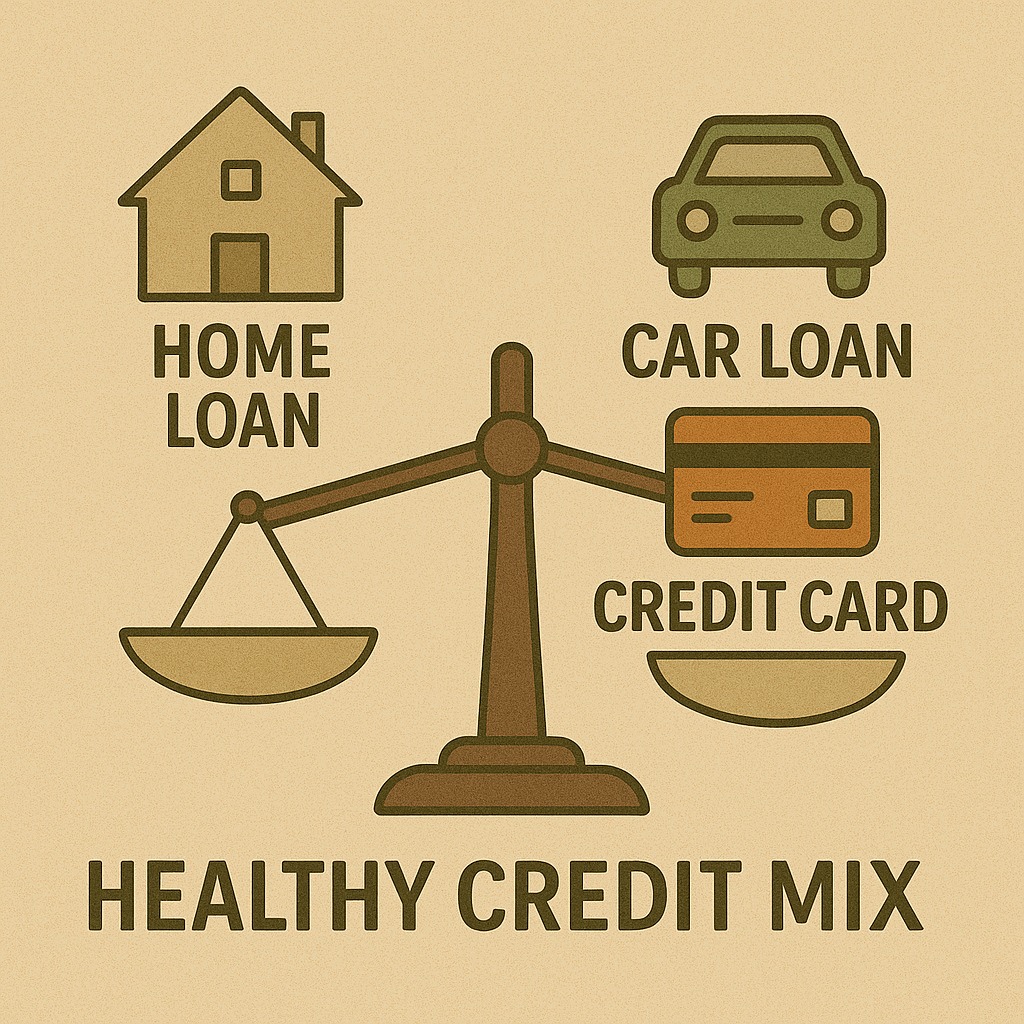

Your credit mix refers to the variety of credit accounts you have — such as credit cards, personal loans, car loans, or a home loan. A diverse credit portfolio signals to lenders that you can handle different types of financial obligations responsibly.

Let’s decode why having more than one type of loan can actually help your credit profile and financial credibility.

1️⃣ What Is a Credit Mix?

A credit mix is the blend of credit types reflected in your credit report.

It generally includes:

💳 Revolving Credit: Credit cards or lines of credit where balances vary monthly.

💰 Installment Credit: Fixed-term loans like home loans, car loans, education loans, or personal loans.

Having both types — and managing them well — creates a balanced credit history, which credit bureaus like CIBIL, Experian, or Equifax reward.

2️⃣ Why Does Credit Mix Matter?

Credit bureaus assess how responsibly you handle various forms of debt.

Here’s why a healthy credit mix improves your score:

✅ Shows Financial Versatility: Demonstrates that you can manage both fixed EMIs and flexible spending credit.

✅ Reduces Risk Perception: Lenders see you as a mature borrower, not dependent on one credit form.

✅ Improves Long-Term Credit History: Installment loans (like home loans) extend your credit timeline, strengthening your credit age.

💬 Example:

Two people have similar scores, but one only uses credit cards while the other manages a credit card and a car loan responsibly.

The second person often has a higher credit score because of their balanced mix.

3️⃣ Ideal Credit Mix for an Individual

There’s no one-size-fits-all formula, but a balanced mix often looks like this:

1–2 Credit Cards (kept under 30% utilization)

1 Secured Loan (Home, Car, or Education Loan)

1 Small Personal Loan (if needed, for diversification)

This combination shows that you can handle short-term and long-term credit simultaneously.

✅ Pro Tip:

Don’t take unnecessary loans just to diversify.

Focus on maintaining healthy repayment habits with existing credit.

4️⃣ How the Credit Mix Impacts Your CIBIL Score

Credit mix contributes roughly 10–15% of your overall credit score calculation in India.

Even if you pay all EMIs on time, a poor mix (like only revolving credit) might slightly limit your score growth potential.

A healthy mix helps you:

Qualify for premium credit cards

Get lower interest rates on loans

Boost lender trustworthiness

Think of it as showing lenders:

“I can handle any kind of credit — big or small — with the same discipline.”

5️⃣ The Risks of an Unbalanced Credit Mix

While variety helps, over-diversification or mismanagement can backfire.

Avoid:

❌ Taking multiple personal loans at once

❌ Overusing credit cards beyond 30% limit

❌ Closing long-term loans too early (reduces credit age)

Balance is key — manage credit smartly, not excessively.

Final Thoughts

Your credit mix is like your financial résumé — it tells lenders how well you manage different responsibilities.

A diverse but disciplined credit portfolio not only strengthens your credit score but also gives you financial flexibility and bargaining power in the future.

The goal isn’t to borrow more — it’s to borrow wisely, build credibility, and keep your financial profile healthy.

Because when managed right, credit isn’t a trap — it’s a tool for financial growth.

❓ Frequently Asked Questions (FAQ)

1. What is a good credit mix?

A good credit mix includes both secured loans (like home or car loans) and unsecured credit (like credit cards or personal loans), all managed responsibly.

2. How much does credit mix affect my CIBIL score?

It contributes about 10–15% of your score. While not the largest factor, it can make a difference if you already have a good payment history.

3. Can I improve my credit score by taking more loans?

No. Simply having multiple loans won’t help — repayment discipline and low credit utilization matter far more.

4. Is it bad to have only one type of credit?

Not necessarily, but it may limit your credit growth. A healthy mix can help demonstrate your ability to manage both revolving and installment debt.

5. Should I close old loans once they’re repaid?

Avoid closing very old credit accounts right away. They add to your credit age, which positively influences your score.

Published on : 8th November

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed