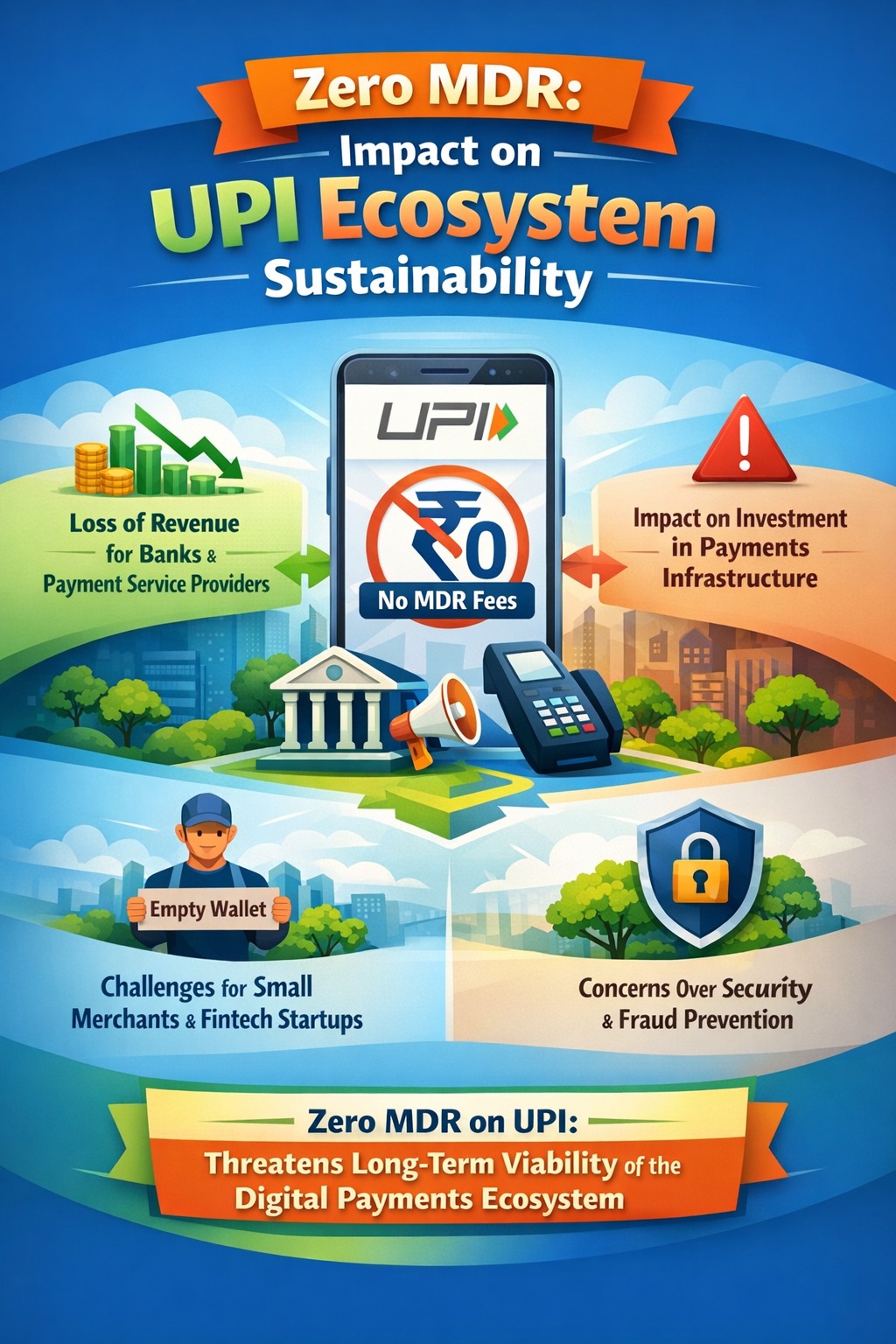

A parliamentary finance panel has raised serious concerns over the zero Merchant Discount Rate (MDR) policy on UPI transactions, warning that it could impact the long-term sustainability of India’s digital payments ecosystem.

The Unified Payments Interface (UPI) has become the backbone of India’s digital economy, enabling billions of transactions every month. However, the absence of MDR charges means banks and fintech companies earn little to no revenue from these transactions.

The panel’s concerns highlight a growing debate: Can India’s digital payment ecosystem remain sustainable without a viable revenue model?

AI Answer Box

What is the issue with zero MDR on UPI?

Zero MDR means merchants do not pay fees on UPI transactions, reducing revenue for banks and fintech firms, raising sustainability concerns.

Key Highlights

| Topic | Details |

|---|---|

| Policy | Zero MDR on UPI |

| Concern | Revenue loss for ecosystem |

| Affected | Banks & fintech companies |

| Outcome | Sustainability challenges |

What Is MDR (Merchant Discount Rate)?

MDR is a fee charged to merchants for processing digital payments.

How MDR Works

Paid by merchants to banks/payment providers

Covers transaction processing costs

Supports payment infrastructure

In most payment systems, MDR is a key revenue source.

What Is Zero MDR Policy?

Under the zero MDR policy:

Merchants are not charged for UPI transactions

Payments remain free for users and businesses

Government promotes digital adoption

While this policy boosted adoption, it created revenue challenges.

Why the Panel Is Concerned

1. Revenue Loss for Banks & Fintech

Banks and payment apps incur costs but earn minimal revenue.

Impact

| Entity | Effect |

|---|---|

| Banks | Reduced income |

| Fintech companies | Profitability pressure |

| Payment infrastructure | Funding challenges |

2. Sustainability of UPI Ecosystem

Maintaining and scaling UPI requires continuous investment.

Without MDR:

Infrastructure costs rise

Innovation may slow

Smaller players may struggle

3. Dependence on Government Support

The government currently provides incentives to support UPI.

However:

Subsidies may not be sustainable long-term

Private sector participation may weaken

Impact on Digital Payment Industry

Positive Effects of Zero MDR

Massive UPI adoption

Increased digital transactions

Financial inclusion growth

Negative Effects

Lack of revenue model

Pressure on fintech startups

Reduced incentives for innovation

Role of Key Institutions

The digital payments ecosystem involves:

Reserve Bank of India

National Payments Corporation of India

Banks and fintech companies

These entities must balance growth and sustainability.

Possible Solutions Being Discussed

Potential Policy Options

Introducing limited MDR for large merchants

Government subsidies for small transactions

Alternative revenue models for fintech firms

These options aim to balance user affordability and ecosystem sustainability.

Expert Commentary

Financial experts believe that while zero MDR has driven adoption, a sustainable revenue model is essential.

Key insights:

Free systems are difficult to sustain long-term

Innovation requires financial incentives

Balanced pricing models may be needed

Experts suggest a gradual transition rather than sudden policy changes.

Future Outlook

The future of UPI depends on how policymakers address these concerns.

Expected Developments

Policy review on MDR structure

New fintech monetization models

Continued growth in digital payments

India must balance affordability, innovation, and sustainability.

Key Takeaways

Zero MDR policy has boosted UPI adoption.

Parliamentary panel raises sustainability concerns.

Banks and fintech firms face revenue challenges.

A balanced revenue model may be needed.

UPI’s future depends on policy decisions.

Frequently Asked Questions (FAQs)

1. What is MDR in digital payments?

A fee charged to merchants for processing transactions.

2. What is zero MDR policy?

Merchants are not charged for UPI transactions.

3. Why is zero MDR a concern?

It reduces revenue for banks and fintech firms.

4. Who raised concerns about MDR?

A parliamentary finance panel.

5. Does zero MDR affect users?

No, payments remain free for users.

6. What is UPI?

A real-time payment system in India.

7. Who manages UPI?

The National Payments Corporation of India.

8. Can zero MDR impact fintech companies?

Yes, it affects their profitability.

9. Are banks affected by zero MDR?

Yes, they lose a potential revenue stream.

10. Will MDR be introduced in future?

Possible policy changes are being discussed.

11. Why is UPI popular?

It is fast, free, and easy to use.

12. What is fintech?

Technology-driven financial services.

13. Can UPI survive without MDR?

It depends on alternative revenue models.

14. What is the role of RBI?

It regulates payment systems.

15. What is the future of digital payments in India?

Strong growth with evolving policies.

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process.

Need quick funds? Apply now at www.vizzve.com

Published on : 20th March

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed