Many people assume that as long as they pay their credit card bill on time, their credit score will stay strong.

But lenders look much deeper than just timely payments — and one major factor that can harm your loan eligibility is high credit card utilisation.

Even if you never miss a due date, using too much of your card limit can make banks consider you a high-risk borrower, especially in 2025–26, where lenders have tightened approval criteria for home loans, personal loans and credit cards.

Here’s why high usage matters and how it impacts your chances of getting a loan.

1. High Utilisation Signals Credit Dependency

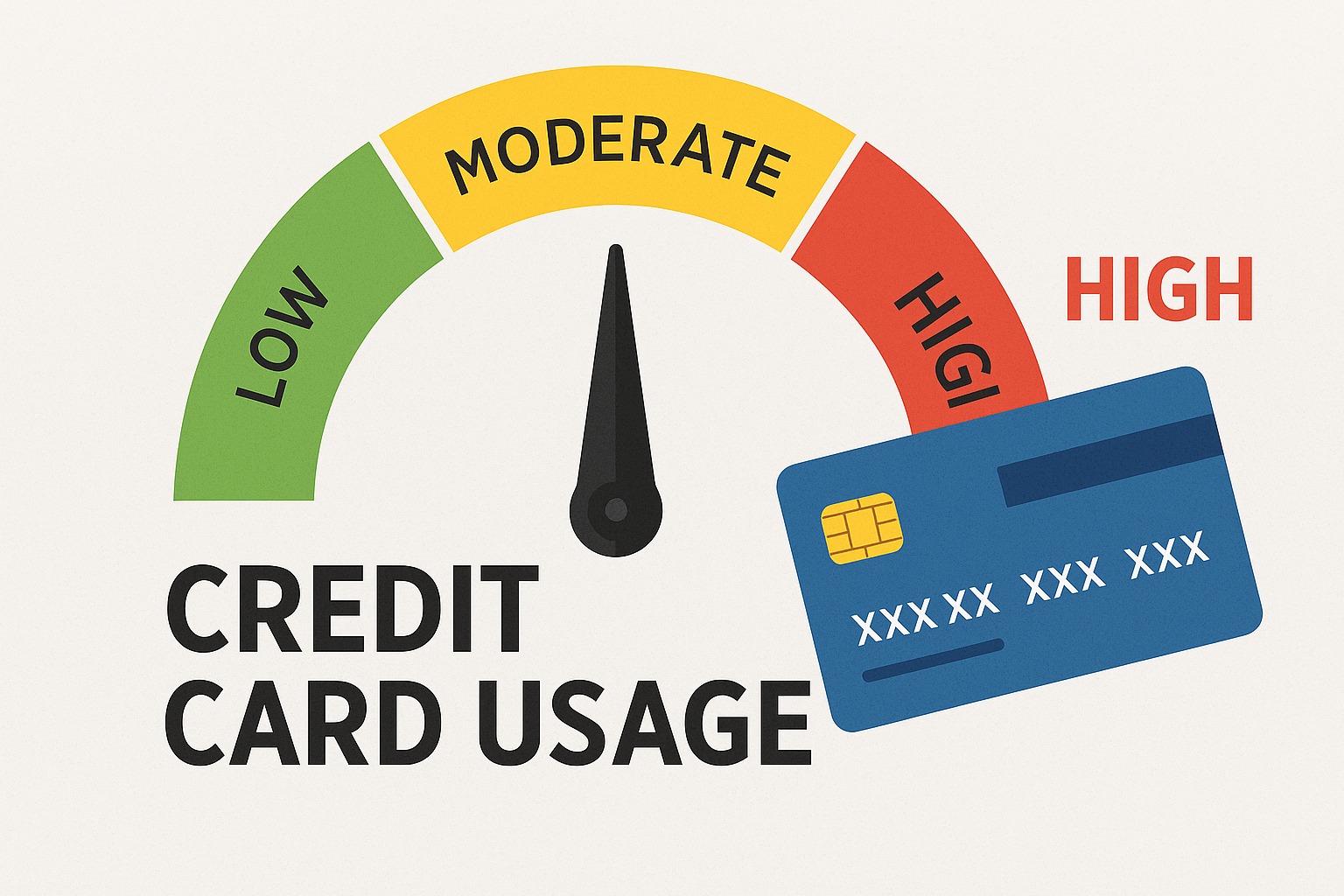

Credit card utilisation refers to the percentage of your available limit you use.

For example:

Card limit: ₹1,00,000

Usage: ₹70,000 → Utilisation = 70%

Anything above 30% is considered high usage.

Banks treat high utilisation as a sign of:

Financial stress

Heavy spending

Dependency on borrowed money

Low savings buffer

This increases your risk rating — which lowers loan eligibility.

2. It Directly Lowers Your Credit Score

Credit utilisation is nearly 30% of your credit score calculation.

When you continuously use more than 40–50% of your limit, your score can drop by 20–60 points even if you pay bills on time.

A lower score means:

Higher interest rates

Stricter scrutiny

Low approval chances

Smaller loan amounts

For big loans like home loans, utilisation plays a major role in lender decisions.

3. Increases Your Debt-to-Income Ratio (DTI)

Banks calculate how much of your income goes towards:

Existing EMIs

Credit card payments

Other debts

If your utilisation is high, your credit card bill becomes large, increasing your DTI ratio.

A high DTI tells banks that you have limited capacity to handle new EMIs.

4. Reduces Your Loan Amount Eligibility

With high utilisation, lenders may:

Approve a smaller loan amount

Offer a shorter tenure

Charge higher interest

Reduce top-up loan eligibility

Even a strong income profile gets affected if utilisation remains consistently high.

5. Creates a Negative Spending Pattern in Your Report

Your credit report shows lenders:

Monthly credit usage

High-value transactions

Consistent over-spending patterns

Revolving balances

If your usage stays at 60–80% every month, lenders interpret it as risky behaviour — lowering your approval chances.

6. Suggests Lack of Cash Flow Stability

High usage implies:

Insufficient savings

Dependence on borrowed funds

Inability to manage expenses within income

Banks prefer borrowers who maintain stable cash flow.

High usage weakens your financial profile significantly.

7. Can Lead to Higher Interest on Loans

Even if banks approve your application, high utilisation often leads to:

Increased interest rates

Reduced offers

No special discounts

Tougher lending terms

Because lenders categorize you under a higher-risk slab.

How to Improve Loan Eligibility Immediately

✔ Maintain utilisation below 30%

✔ Ask for a limit increase (if income supports it)

✔ Split expenses across 2–3 cards

✔ Pay twice a month to keep utilisation low

✔ Avoid large purchases before loan applications

✔ Clear full bill, never revolve credit

Keeping utilisation low for 2–3 months can increase both your credit score and loan eligibility.

FAQs

Q1. What is the ideal credit utilisation for loan approval?

Below 30% is considered the safest range.

Q2. Does high usage matter even if I pay on time?

Yes. Utilisation affects your score separately from payment history.

Q3. How fast does utilisation impact credit score?

It reflects in the next monthly reporting cycle.

Q4. Do banks check monthly usage or yearly average?

Most lenders analyse recent 3–6 month usage patterns.

Q5. Can reducing utilisation improve my loan eligibility?

Yes, improved utilisation boosts both credit score and lender confidence.

Published on : 15th November

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed