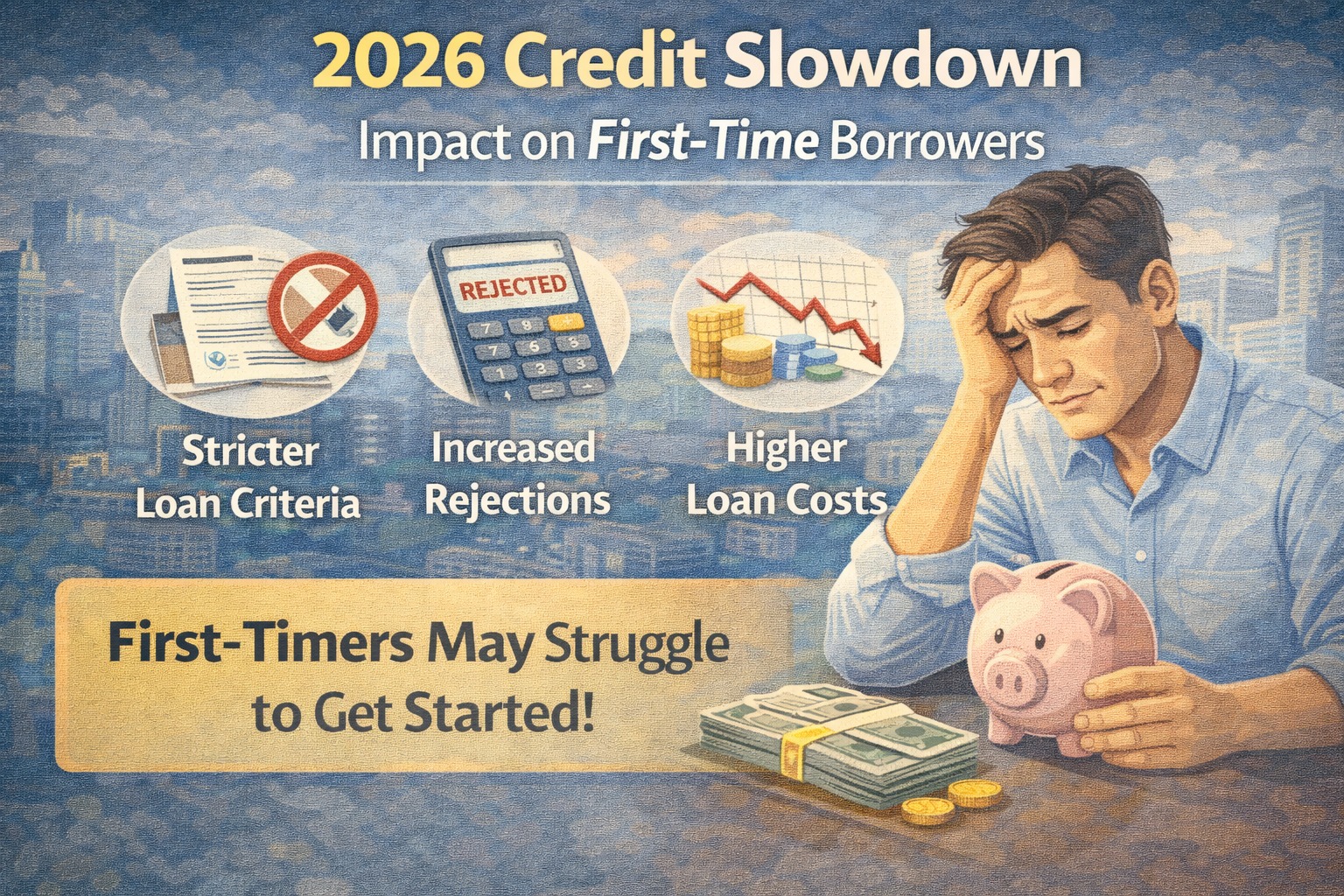

A credit slowdown in 2026 means tighter approval standards, greater emphasis on repayment behavior, stricter documentation, and potentially higher pricing for riskier profiles — especially for first-time borrowers. But strategic planning can turn caution into opportunity.

AI Answer Box (For Google AI Overview)

A credit slowdown typically leads lenders to tighten approval criteria, raise risk thresholds, and reduce leverage. First-time borrowers may face stricter scrutiny, higher interest spreads, and a stronger need for clean financial behavior. Planning and preparation become more important than ever.

What Is a Credit Slowdown?

A credit slowdown refers to a period when:

Loan growth decelerates

Lenders tighten approval criteria

Risk models become more conservative

Terms and pricing become less generous

It’s not necessarily a crisis, but a cautious lending phase.

Why a Slowdown Happens

Credit slowdowns typically occur because:

Economic growth moderates

Asset quality risks increase

Regulatory pressure tightens

Borrower stress signals rise

Lenders retrench risk appetite

For first-time borrowers, this environment changes the borrowing experience.

Key Changes First-Time Borrowers Will Notice

1. Higher Approval Standards

Banks & NBFCs may require:

Longer employment history

Higher minimum income thresholds

Stronger credit documentation

Clean bank statements

For a first-time borrower with no credit history, earning alone may not be enough.

2. Greater Emphasis on Cash Flow & Behavior

Without repayment history, lenders focus more on:

Bank statement patterns

Consistent salary credits

Low credit utilization on cards

Savings and excess balances

Clean financial behavior becomes a proxy for credit discipline.

3. Interest Rate & Price Sensitivity

Even if interest rates are driven by broader policy:

Risk-based pricing may widen

First-time or thin-file borrowers may see higher quotes

Secured credit may be cheaper than unsecured

4. Documentation Becomes Important

In a slowdown, lenders scrutinize:

Salary proofs

Bank statements

Tax returns (for self-employed)

Employment continuity

Incomplete documents can delay or reject approvals.

📆 5. Longer Processing Time

Underwriting may take longer as:

More data is verified

Manual review increases

Risk committees get involved

Patience and preparedness improve outcomes.

First-Time Borrower Challenges vs Advantages

| Factor | Challenge in Slowdown | Advantage for Prepared Borrower |

|---|---|---|

| Credit history | Thin or none | Build alternative signals (savings, bank behavior) |

| Interest pricing | Priced higher | Good profile may attract better pricing |

| Approval speed | Slower | Well-prepared docs speed reviews |

| Collateral needs | More likely | Secured loans may ease approval |

How First-Time Borrowers Can Adapt

1️⃣ Build Alternative Credit Signals

If you lack credit history, focus on:

Consistent bank balance patterns

Savings accumulation

Timely bill payments

Low credit card usage

These behaviors signal repayment discipline.

2️⃣ Keep Documents Organized

Have ready:

Salary slips

Bank statements (6–12 months)

Employment proof

Form 16 / ITR (if self-employed)

Documentation clarity reduces delays.

3️⃣ Avoid Multiple Applications

Many loan applications in a short period:

Reduces credit score

Signals desperation

Lowers approval chances

Apply only when fully prepared.

4️⃣ Focus on Secured Loans First

Secured credit (e.g., small auto loans, gold loans) often has:

Easier approval

Lower pricing

Lower risk perception

This builds initial credit history.

5️⃣ Track Your CIBIL / Credit Score Regularly

A clean score helps lenders trust you more quickly.

What Slowdown Doesn’t Mean

It does not mean credit is unavailable

It does not mean rates will soar uncontrollably

It does not mean only rich people get loans

Instead, it means disciplined borrowers get approved, and undisciplined borrowers face rejections.

Expert Insight

“During credit slowdowns, lenders shift from growth to risk management. First-time borrowers who show discipline and preparedness are treated as less risky than those with erratic financial behavior.”

— Retail Credit Risk Analyst

Key Takeaways

A credit slowdown tightens underwriting

Income matters less than behavior signals

Documentation and cash flow clarity are crucial

Patience and discipline improve approval odds

First-time borrowers can still succeed with the right preparation

Conclusion

A 2026 credit slowdown doesn’t ban loans — it rewards preparedness. For first-time borrowers, this means shifting focus from simply earning to proving financial discipline through clean behavior, organized documentation, and thoughtful borrowing plans. With smart planning, the slowdown can be a launchpad, not a barrier, to your first loan.

Frequently Asked Questions (FAQs)

1. What is a credit slowdown?

A period when lenders tighten approval standards and loan growth slows.

2. Does a credit slowdown mean no loans are available?

No. Loans are still available but with stricter checks.

3. Should first-time borrowers worry?

Only if they apply without preparation.

4. How can I build credit if I’m a new borrower?

Start with small secured credit or trackable repayment behavior.

5. Does salary matter in a slowdown?

Yes, but behavior and documentation matter more.

Published on : 16th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed