Paying your personal loan EMIs on time is essential to maintaining a good financial record. However, if your EMI bounces due to insufficient balance, bank issues, or technical errors, it can lead to penalties, higher costs, and a drop in your credit score.

At Vizzve Finance, we believe in promoting responsible borrowing and helping customers understand what happens when an EMI fails — and how to avoid it in the future.

What Does an EMI Bounce Mean?

An EMI bounce occurs when your scheduled loan payment fails to process — usually because of insufficient funds in your bank account, an expired mandate, or technical errors during auto-debit.

When this happens, your lender may charge a bounce penalty, and the missed payment will be reported to credit bureaus, potentially affecting your credit profile.

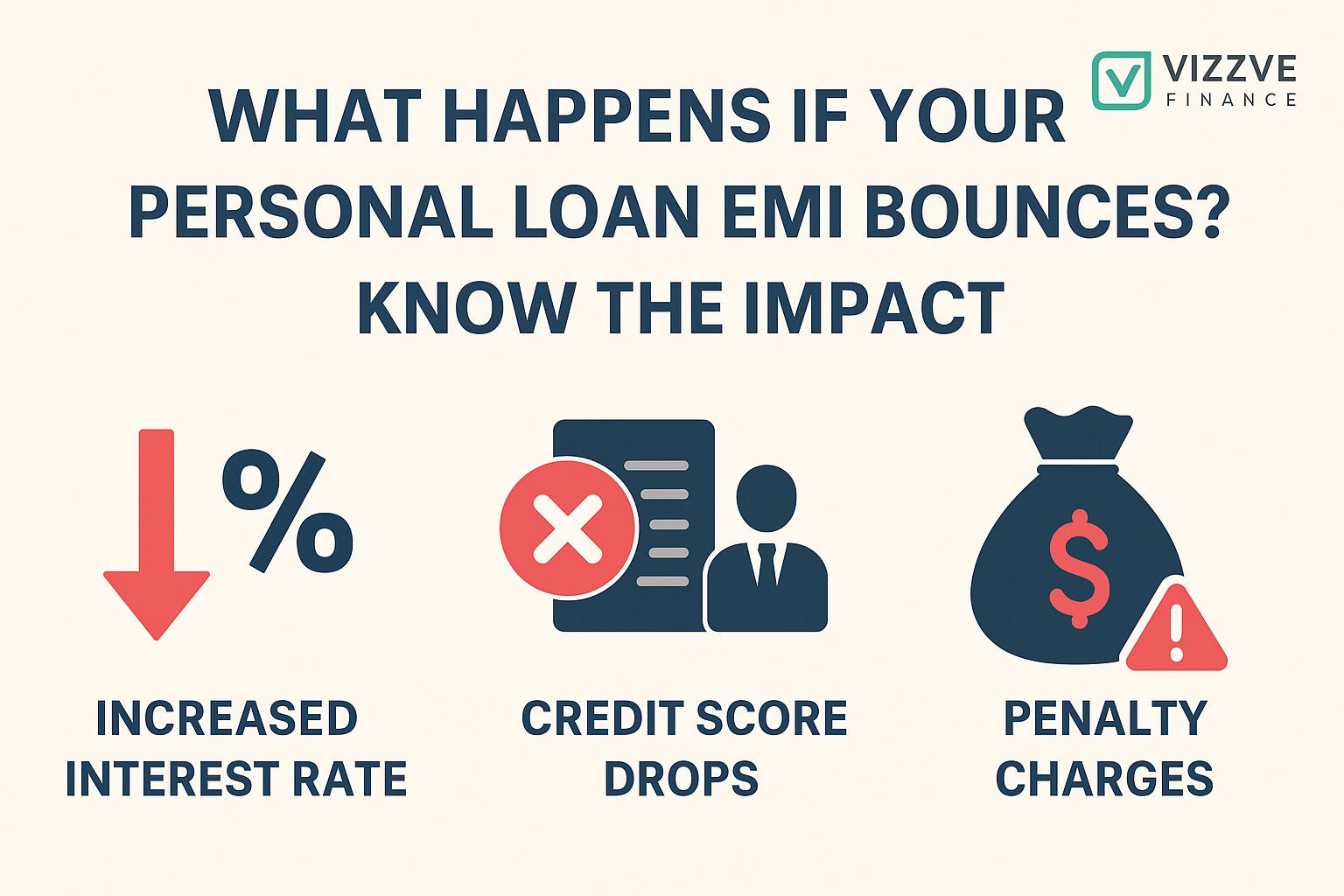

Consequences of a Personal Loan EMI Bounce

1. Penalty Charges

Banks and lenders usually impose penalty fees ranging from ₹200 to ₹1,000 for every missed EMI.

In addition, late payment interest may apply until you clear the dues.

2. Credit Score Impact

Even a single missed EMI can lower your credit score by 50–100 points.

Multiple bounces can make it harder to get loans in the future, as lenders see it as a sign of poor repayment discipline.

3. Legal and Collection Action

If EMIs bounce repeatedly, lenders can issue legal notices or involve collection agencies.

Continuous default may also lead to the loan being marked as an NPA (Non-Performing Asset).

4. Difficulty Getting Future Loans

When lenders notice EMI bounces in your credit history, they may reject your future loan or credit card applications.

With Vizzve Finance, maintaining a consistent repayment record ensures easy access to future micro or personal loans when needed.

Common Reasons for EMI Bounce

Insufficient bank balance on the due date.

Outdated auto-debit mandate (NACH or ECS).

Technical glitches in payment systems.

Salary delays or unexpected expenses.

Regardless of the cause, prompt correction helps you maintain financial discipline.

How to Avoid EMI Bounce

Maintain sufficient balance before the due date.

Set up auto-debit reminders on your phone or calendar.

Choose a convenient EMI date aligned with your salary cycle.

Monitor your loan account regularly.

Inform your lender early if you’re facing a temporary financial issue.

Vizzve Finance also offers flexible repayment options for short-tenure loans, helping borrowers avoid EMI stress.

What to Do If Your EMI Has Already Bounced

Pay the due amount immediately along with the penalty.

Check your credit report for any negative entry.

Contact your lender to discuss possible solutions or a rescheduled plan.

Being proactive helps limit the long-term impact on your creditworthiness.

Final Thoughts

An EMI bounce might seem minor, but it can seriously affect your financial reputation if ignored. Always stay alert, maintain sufficient balance, and manage payments wisely.

At Vizzve Finance, we encourage smart borrowing habits through transparent processes, short-tenure micro loans, and timely reminders — ensuring you stay in control of your financial commitments.

FAQs

Q1: How many EMI bounces are allowed before action is taken?

Usually, lenders take strict action after two or more consecutive EMI bounces.

Q2: Does one EMI bounce affect my credit score?

Yes. Even a single missed EMI can reduce your score temporarily.

Q3: Can I change my EMI date to avoid bounce issues?

Yes. Many lenders, including Vizzve Finance, allow EMI date changes upon request.

Q4: What should I do if I miss an EMI due to technical issues?

Immediately inform your lender and make a manual payment to avoid penalty or credit impact.

Published on : 4th November

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed