A loan becomes NPA after 90 days of missed EMIs. Before this happens, borrowers should communicate with the lender, restructure EMIs, seek moratorium or tenure extension, and protect their credit report. Early action can prevent long-term financial damage.

AI Answer Box

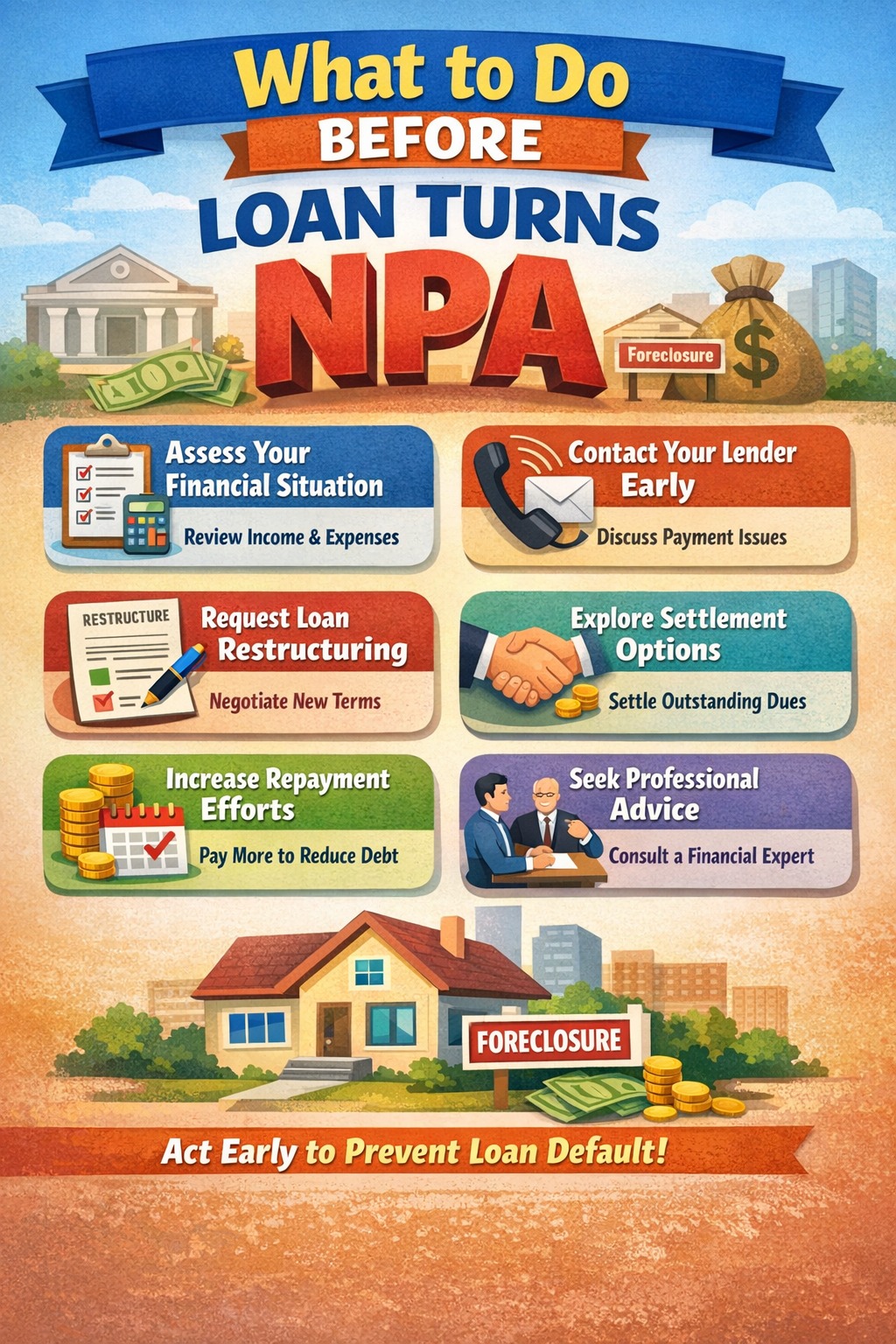

What to do before loan becomes NPA:

Act within first missed EMI

Inform lender immediately

Request restructuring or relief

Avoid ignoring calls/notices

Protect credit score early

🔹 Introduction

Missing one EMI is stressful. Missing two feels alarming. But once a loan crosses 90 days overdue, it officially becomes an NPA (Non-Performing Asset)—a stage where consequences escalate sharply.

Many borrowers don’t realize that the window before NPA is your most powerful opportunity. Acting early can save your credit score, reduce penalties, and even protect you from legal action.

This guide explains exactly what to do before your loan turns NPA—step by step.

🔹 What Is an NPA? (Simple Explanation)

A loan is classified as NPA when:

EMI remains unpaid for 90 consecutive days

Interest or principal is overdue beyond 90 days

This applies to:

Home loans

Personal loans

Business loans

Credit cards

As per the Reserve Bank of India, NPA classification is mandatory for banks and NBFCs.

🔹 NPA Timeline: When Trouble Starts

| Days Overdue | Loan Status | Risk Level |

|---|---|---|

| 1–30 days | Overdue | Low |

| 31–60 days | SMA-1 | Medium |

| 61–90 days | SMA-2 | High |

| 90+ days | NPA | Severe |

📌 Action before 60 days is critical.

🔹 Early Warning Signs Your Loan Is at Risk

Salary/business income disruption

Using credit cards to pay EMIs

Ignoring bank messages

Multiple EMIs consuming income

Frequent late fees and penalties

Recognizing stress early prevents collapse.

🔹 Step-by-Step: What to Do Before Loan Turns NPA

✅ Step 1: Don’t Ignore the First Missed EMI

One missed EMI hurts—but silence hurts more.

Pay partial amount if possible

Inform lender proactively

Avoid repeated delays

✅ Step 2: Contact Your Lender Immediately

Banks prefer resolution over default.

Ask about:

Temporary EMI reduction

Payment rescheduling

Grace period or short moratorium

📌 Communication builds trust.

✅ Step 3: Request Loan Restructuring (If Needed)

Restructuring may include:

Tenure extension

EMI reduction

Temporary interest-only payments

This is far better than defaulting.

✅ Step 4: Prioritise EMI Over Other Expenses

Before NPA:

Pause discretionary spending

Avoid new loans

Use emergency savings wisely

Saving your credit profile should be priority #1.

✅ Step 5: Avoid Settlements Before NPA

Settlement before NPA:

Permanently damages credit report

Signals financial distress

Settlements should be last-resort, not first action.

✅ Step 6: Keep Proof of All Payments & Communication

Maintain:

Payment receipts

Emails/messages with bank

Call logs

These help if disputes arise later.

🔹 What Happens If You Ignore the Problem?

If loan becomes NPA:

Credit score drops sharply

Recovery calls intensify

Legal notices may follow

Settlement/write-off risk rises

Prevention is always cheaper than recovery.

🔹 Can EMI Relief or Moratorium Help?

Sometimes, yes—especially during:

Job loss

Medical emergencies

Temporary business slowdown

Banks assess intent + ability to repay.

🔹 Borrower Rights Before Loan Becomes NPA

You have the right to:

Know outstanding dues

Request restructuring

Receive fair communication

Avoid harassment

Regulated lenders must follow RBI conduct rules.

🔹 Real-World Borrower Insight

From loan stress cases, borrowers who approach banks within 30–45 days of stress often avoid NPA entirely, while those who wait till 80–90 days face long-term damage—even if income recovers later.

➡️ Timing matters more than amount.

🔹 Pros & Cons of Early Action

✅ Pros

Credit score protection

Lower penalties

Better negotiation power

❌ Cons

Temporary lifestyle adjustment

Longer loan tenure

🔹 Key Takeaways

NPA starts after 90 days overdue

Early action can prevent NPA

Communication with lender is critical

Restructuring is better than default

Credit behaviour defines future access

🔹 Frequently Asked Questions (FAQs)

1. When does a loan become NPA?

After 90 days of non-payment.

2. Can one missed EMI make loan NPA?

No, but repeated misses can.

3. Does NPA affect credit score?

Yes, severely.

4. Can I stop loan from becoming NPA?

Yes, with early action.

5. Is restructuring bad for credit score?

Less harmful than NPA.

6. Should I ignore recovery calls?

No, communicate.

7. Can banks take legal action before NPA?

Usually after NPA.

8. Is settlement better than restructuring?

No.

9. Can I take another loan to pay EMI?

Risky—avoid.

10. Does RBI protect borrowers?

Yes, via fair practice norms.

11. How fast does credit score fall after NPA?

Immediately.

12. Is NPA permanent?

No, but recovery takes years.

🔹 Conclusion + CTA

A loan turning NPA is not a sudden event—it’s a process. Borrowers who act early, communicate honestly, and choose restructuring over silence can avoid years of financial damage.

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process. Apply at www.vizzve.com.

Published on : 8th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed