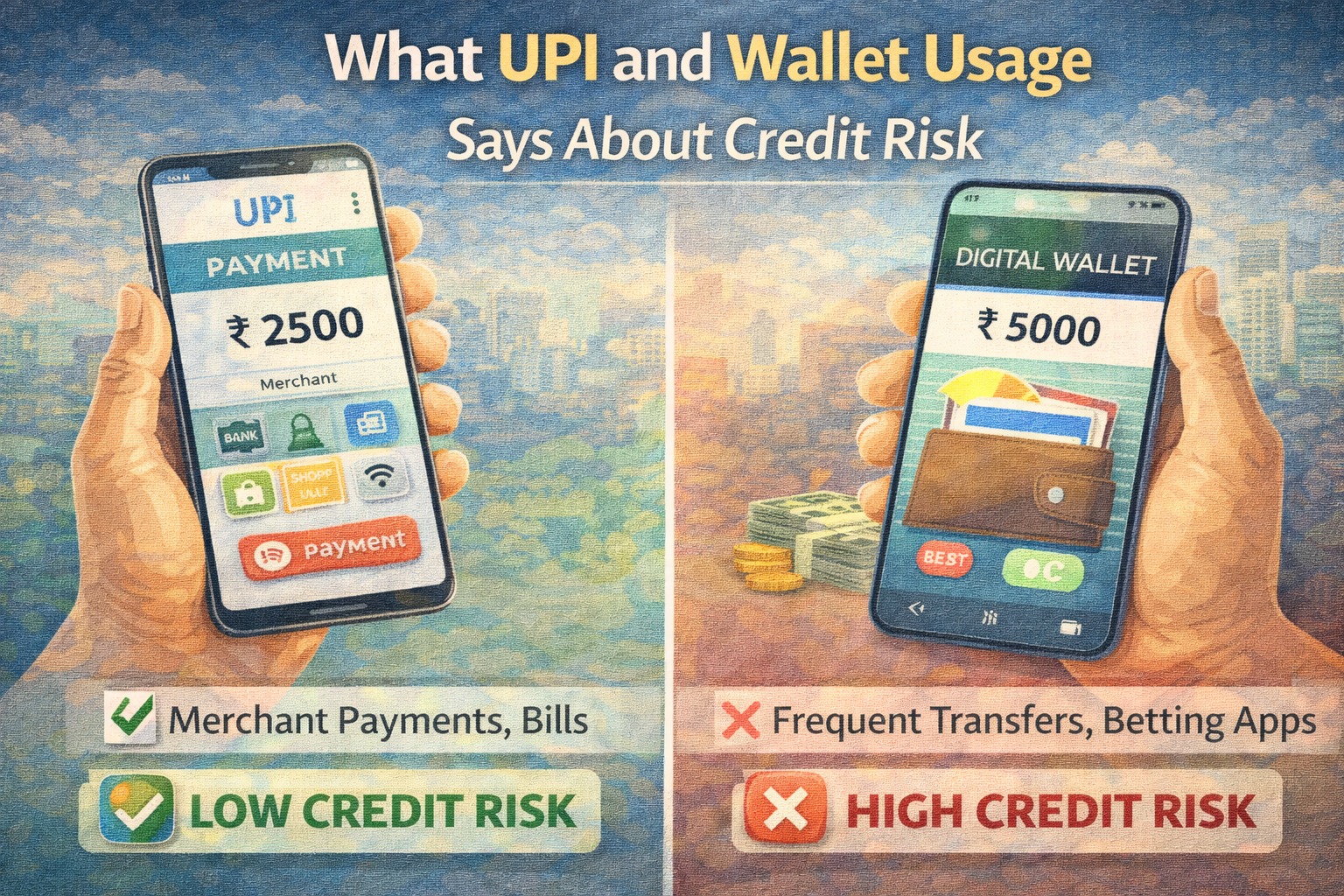

Your UPI and wallet usage shows spending discipline, cash-flow stability, and repayment behavior—signals lenders increasingly use to assess credit risk, especially for digital and first-time borrowers.

AI Answer Box (For Google AI Overview & AI Search)

UPI and wallet transactions reflect real-time money behavior. Frequent low balances, excessive micro-spending, overdraft patterns, and irregular income flows can signal higher credit risk, while stable balances and disciplined usage improve lender confidence.

Why Digital Payments Matter in Credit Decisions

Earlier, banks relied mainly on:

Salary slips

Credit score

Past EMIs

Today, lenders also analyze digital payment behavior because it shows:

Daily money discipline

Real spending habits

Cash-flow stress signals

UPI and wallets act like a financial mirror.

What Lenders Learn From Your UPI Usage

1️⃣ Spending Discipline

Too many impulsive transactions:

Food delivery

Quick commerce

Gaming or entertainment

can indicate uncontrolled spending behavior, even if income is stable.

2️⃣ End-of-Day & End-of-Month Balance

UPI debits that:

Drain balance to near zero daily

Leave no buffer before salary credit

signal tight cash flow, a key risk indicator.

3️⃣ Transaction Frequency Patterns

Thousands of micro-transactions may suggest:

No budgeting discipline

Living paycheck to paycheck

Balanced usage reflects planned spending.

4️⃣ Failed Transactions & Declines

Repeated failed UPI transactions:

Indicate insufficient balance

Signal poor fund management

These are silent but powerful risk flags.

What Wallet Usage Reveals

1️⃣ Dependency on Wallet Credit

Using wallet-based credit frequently suggests:

Short-term liquidity stress

Dependence on small-ticket borrowing

This can raise risk perception.

2️⃣ Cashback-Chasing Behavior

Constant wallet switching for offers:

Indicates transaction-driven behavior

Sometimes correlates with impulsive spending

3️⃣ Wallet Balance Management

Keeping:

Zero wallet balance most days

Or topping up repeatedly in small amounts

shows reactive money management.

Healthy vs Risky Digital Payment Behavior

| Behavior | Low Credit Risk | High Credit Risk |

|---|---|---|

| UPI usage | Planned & regular | Excessive & impulsive |

| Wallet dependency | Occasional | Frequent |

| Balance pattern | Stable buffer | Near zero |

| Failed transactions | Rare | Frequent |

| Spend categories | Balanced | Mostly discretionary |

Why This Matters More in 2026

In tighter credit cycles:

Lenders seek alternate data

Digital footprints fill gaps for:

First-time borrowers

Thin credit profiles

Gig and self-employed users

UPI behavior often acts as a credit proxy.

What Digital Lenders Especially Watch

Digital lenders analyze:

UPI debit-to-credit ratio

Average daily balance

Frequency of discretionary spends

Wallet credit usage

Spending consistency across months

This data feeds automated risk models.

Expert Insight

“Digital payments reveal how people actually live with money. In the absence of long credit history, UPI behavior becomes a strong indicator of repayment discipline.”

— Fintech Risk Analyst

How to Improve Your UPI & Wallet Credit Signals

✅ 1. Maintain a Daily Balance Buffer

Aim for 1–2 weeks of expenses as balance.

✅ 2. Reduce Micro-Impulse Spending

Bundle payments and avoid excessive small transactions.

✅ 3. Avoid Wallet Credit Overuse

Treat wallet credit like a loan, not free money.

✅ 4. Keep Transactions Clean & Predictable

Consistency builds trust in risk models.

✅ 5. Review Digital Spending Monthly

Awareness itself improves behavior.

Common Myths (Busted)

❌ “UPI data doesn’t matter”

✅ It increasingly does

❌ “Only credit score is checked”

✅ Digital behavior supplements score

❌ “Small spends don’t show risk”

✅ Patterns matter more than amounts

Key Takeaways

UPI usage shows real financial behavior

Wallet dependency can signal liquidity stress

Stable balances improve credit perception

Digital discipline supports loan approval

Small habits create big credit signals

Conclusion

Your UPI and wallet usage quietly tells lenders how you handle money daily. In a world where credit decisions are increasingly data-driven, digital payment discipline is becoming as important as EMI history. By managing balances, reducing impulsive spending, and using wallets responsibly, borrowers can strengthen their credit profile—often without realizing it.

❓ Frequently Asked Questions (FAQs)

1. Does UPI usage really affect credit risk?

Indirectly, yes. UPI usage shows spending discipline and cash-flow behavior, which lenders increasingly analyze—especially for digital loans.

2. Do banks actually look at wallet transactions?

Yes. Wallet and UPI transactions are visible through bank statements or consent-based data sharing, and patterns are assessed.

3. Is using UPI frequently a bad sign?

No. Uncontrolled or impulsive usage patterns, not frequency alone, raise credit risk concerns.

4. Can digital payment behavior replace credit score?

No. It supplements credit score, especially for first-time or thin-file borrowers.

5. Does wallet credit impact my credit score?

Some wallet credit products do, particularly if repayments are delayed or reported to credit bureaus.

6. What kind of UPI behavior looks risky?

Frequent failed transactions, zero balance patterns, excessive micro-spending, and heavy reliance on wallet credit.

7. How many months of UPI data do lenders check?

Typically the last 3–6 months of transaction behavior.

8. Are small UPI payments important?

Yes. Patterns matter more than amounts in risk analysis.

9. Can improving UPI habits improve loan approval chances?

Yes. Cleaner digital behavior improves risk perception and lender confidence.

10. Do first-time borrowers get judged more on UPI usage?

Yes. In the absence of EMI history, UPI behavior becomes a proxy for financial discipline.

Published on : 16th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed