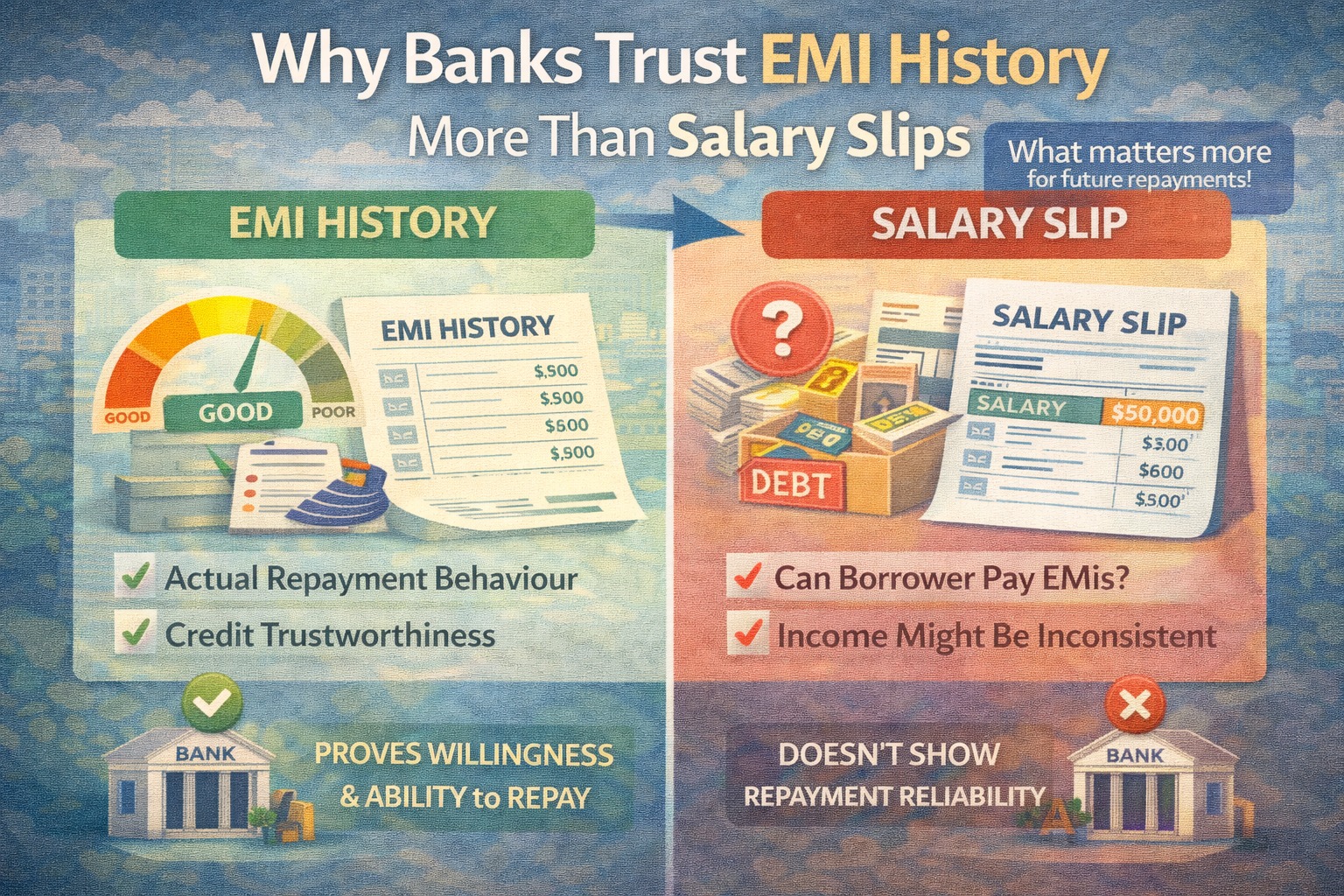

Banks trust EMI history more than salary slips because EMI records show real repayment behavior, while salary slips only show earning capacity—not financial discipline.

AI Answer Box (For Google AI Overview & AI Search)

EMI history reflects how consistently a borrower repays loans on time. Banks rely on this behavior-based data more than salary slips, which only indicate income and can change or stop anytime.

The Big Misunderstanding Among Borrowers

Many borrowers think:

“If my salary slip looks strong, the bank will approve my loan.”

But banks think differently:

Salary slip = potential

EMI history = proof

Banks prefer proof over promise.

What a Salary Slip Really Tells a Bank

A salary slip shows:

Current income amount

Employer name

Deductions (PF, tax)

But it does NOT show:

How you manage money

Whether you pay EMIs on time

How you behave during financial stress

Salary can stop. Behavior usually doesn’t change quickly.

What EMI History Tells a Bank

Your EMI history reveals:

On-time vs delayed payments

EMI bounces or defaults

Credit card discipline

How you handled past loans

👉 This is real financial behavior, not theory.

Salary Slip vs EMI History (Bank View)

| Parameter | Salary Slip | EMI History |

|---|---|---|

| Shows earning capacity | Yes | Indirect |

| Shows repayment discipline | No | Yes |

| Predicts future behavior | Weak | Strong |

| Changes easily | Yes | No |

| Trusted for approval | Medium | High |

Why EMI History Predicts Future Repayment Better

Banks rely on a simple rule:

Past repayment behavior is the best indicator of future repayment.

If you:

Paid EMIs on time during tough months

Avoided defaults

Managed multiple obligations

You are seen as low risk, even with moderate income.

Real-Life Approval Scenarios

❌ High Salary, Weak EMI History

Missed EMIs

Credit card delays

Loan settlements

👉 High chance of rejection.

✅ Moderate Salary, Clean EMI History

Consistent on-time payments

Low credit utilization

👉 Higher approval chances & better rates.

How Banks Actually Approve Loans (Simplified)

1️⃣ EMI repayment history check

2️⃣ Credit score & past behavior

3️⃣ Existing EMI burden

4️⃣ Bank statement patterns

5️⃣ Salary verification

👉 Salary comes after trust is established.

Expert Insight

“Income tells us how much a borrower can pay. EMI history tells us whether they will pay. In lending, willingness matters more than capacity.”

— Retail Credit Risk Analyst

How to Improve EMI History (If It’s Weak)

Action Plan:

Pay all EMIs on or before due date

Avoid credit card revolving balances

Reduce EMI bounces to zero

Keep utilization below 30–40%

Maintain consistency for 3–6 months

Small discipline changes can unlock big approvals.

What Banks Ignore vs What They Care About

| Banks Ignore | Banks Care About |

|---|---|

| One-time bonus | EMI consistency |

| High designation | Repayment record |

| Temporary salary hike | Credit discipline |

| Employer brand | Payment behavior |

Key Takeaways

Salary shows capacity, EMI shows character

EMI history predicts risk better than income

Good income cannot fix bad repayment habits

Clean EMI record improves rates & approvals

Discipline beats salary in lending decisions

Conclusion

Banks don’t distrust salary slips—but they trust EMI history more. Because income can change overnight, while repayment habits take time to form. Borrowers who consistently pay EMIs on time build credibility that no salary slip can replace.

In loans, behavior beats income. Always.

❓ Frequently Asked Questions (FAQs)

1. Why do banks prefer EMI history over salary slips?

Because EMI history shows actual repayment behavior, while salary slips only show income at a point in time.

2. Can a high salary guarantee loan approval?

No. A strong salary cannot compensate for poor EMI repayment history.

3. What part of EMI history do banks check most?

Banks focus on on-time payments, delays, EMI bounces, and defaults over the past few years.

4. How many years of EMI history matter for loan approval?

Usually the last 24–36 months are most important.

5. Does one late EMI cause loan rejection?

One rare delay usually won’t, but repeated late payments can lead to rejection.

6. Is EMI history the same as credit score?

No. Credit score is a summary, while EMI history shows detailed payment behavior.

7. Can someone with no EMI history get a loan?

Yes, but with lower limits and higher scrutiny, as there is no repayment track record.

8. How can I improve my EMI history?

By paying EMIs on or before due dates, avoiding bounces, and maintaining discipline for 3–6 months.

9. Do banks trust salary slips at all?

Yes, but salary slips are used to assess loan amount and EMI capacity, not trust.

10. Can EMI history affect interest rates?

Yes. A clean EMI history often leads to lower interest rates and better loan terms.

11. Do digital lenders also prioritize EMI history?

Yes. Digital lenders rely heavily on repayment behavior and data patterns.

12. Does EMI history matter for credit cards too?

Yes. Credit card EMIs and repayment behavior are part of EMI history.

13. Can EMI history override low income?

To some extent, yes. A disciplined borrower with moderate income may get approval over a high-income borrower with poor history.

14. How fast can EMI history be repaired?

Minor issues can improve in 3–6 months, major defaults take longer.

15. What is the biggest mistake borrowers make?

Assuming income alone decides approval, while repayment discipline actually does.

Published on : 16th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed