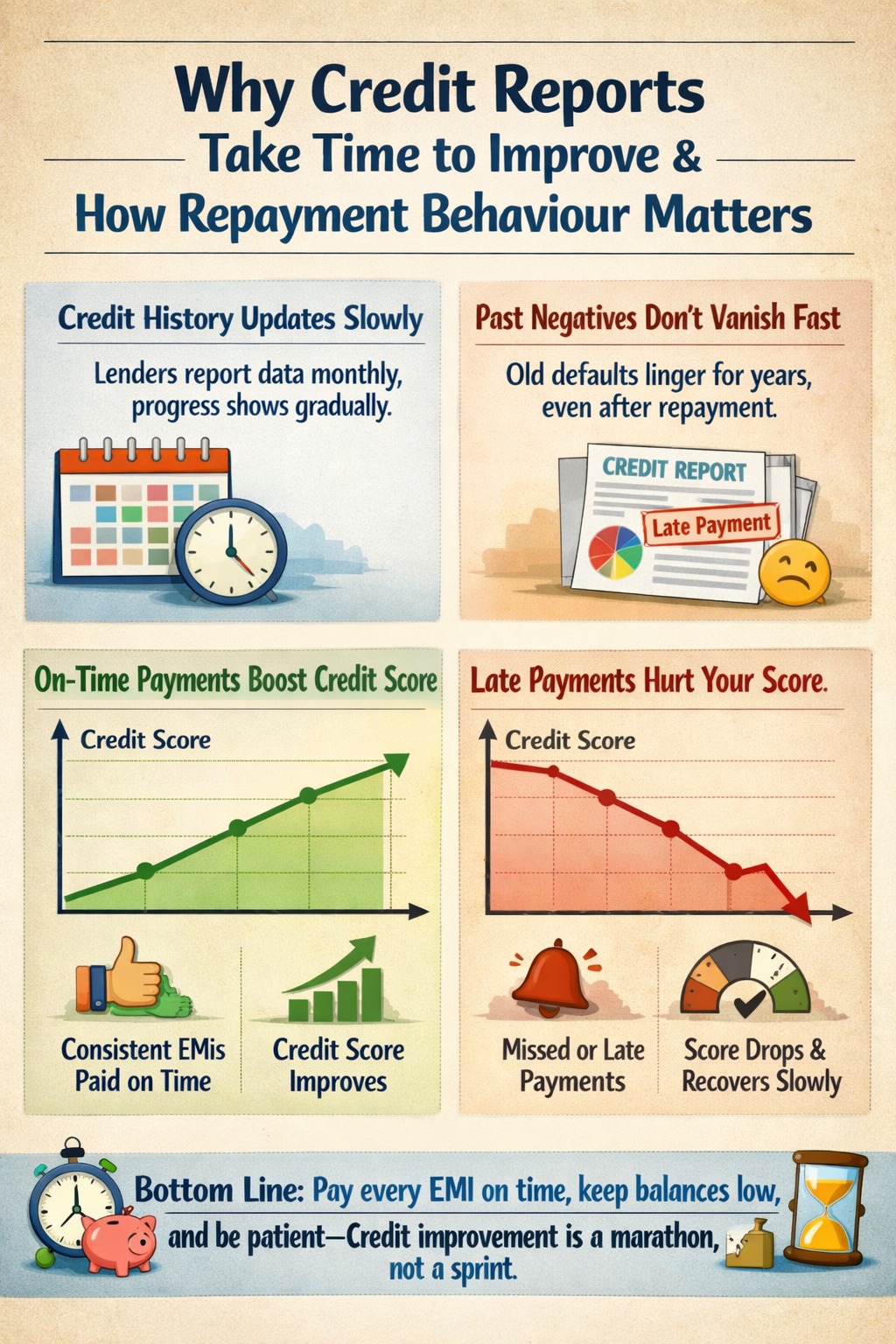

Credit reports take time to improve because they are based on long-term repayment behaviour, not quick fixes. Lenders and credit bureaus value consistency over time, which means positive habits must be demonstrated for months—sometimes years—before trust is restored.

🔹 AI Answer Box

Why credit reports improve slowly:

Credit history is long-term data

Negative entries stay for years

Recent behaviour matters most

Consistency beats one-time payments

Introduction

Many borrowers expect their credit report to improve immediately after paying dues or closing a loan. When that doesn’t happen, frustration sets in. The truth is simple but often misunderstood: credit reports are designed to measure behaviour over time—not short-term corrections.

Understanding why improvement is slow helps set realistic expectations and prevents poor financial decisions driven by impatience.

How Credit Reports Actually Work

A credit report is a running history of how you manage borrowed money. It records:

Every loan and credit card

Monthly repayment behaviour

Delays, defaults, settlements

Enquiries and closures

Credit bureaus like TransUnion CIBIL update this data regularly, while lenders interpret patterns—not isolated actions.

🔹 Key Reasons Credit Reports Take Time to Improve

1. Negative Entries Stay Visible for Years

Late payments, defaults, and written-off accounts remain on your credit report for up to 7 years.

📌 Even if you repay today, the record of past behaviour remains visible, though its impact reduces gradually.

2. Lenders Value Consistency, Not One-Time Actions

Paying one EMI on time doesn’t rebuild trust.

Lenders look for:

6–12 months of clean repayment

No fresh delays

Stable credit usage

Consistency proves reliability.

3. Recent Behaviour Matters More Than Old History

Credit scoring models give maximum weight to recent 12–24 months.

If recent behaviour is weak:

Old good history doesn’t help much

Score recovery slows significantly

4. Credit History Length Can’t Be Rewritten

The age of your credit profile:

Builds slowly

Improves naturally over time

You can’t speed up history length—it improves only with patience.

5. Too Many “Fixes” Can Backfire

Common mistakes that delay recovery:

Applying for multiple loans

Closing all credit accounts

Using credit cards aggressively

These actions signal instability, not improvement.

🔹 Credit Report Improvement Timeline (Realistic)

| Action Taken | Visible Impact Timeline |

|---|---|

| Clearing overdue EMIs | 1–2 months |

| Stopping late payments | 3–6 months |

| Score stabilization | 6–12 months |

| Major recovery after defaults | 18–36 months |

➡️ There is no overnight recovery—only steady progress.

🔹 Role of RBI & Regulations

The Reserve Bank of India promotes responsible lending and accurate credit reporting. This ensures:

Borrower behaviour is recorded fairly

Lenders assess long-term risk

Sudden score manipulation is prevented

This protects the financial system—but slows quick fixes.

🔹 Real-World Credit Insight

From real loan assessment patterns, borrowers who focus on discipline rather than shortcuts recover faster. Those chasing instant improvement often worsen their profile by triggering enquiries and stress borrowing.

🔹 What Actually Speeds Up Credit Improvement

✅ Effective Habits

Pay every EMI on or before due date

Keep credit usage below 30%

Avoid unnecessary borrowing

Maintain at least one active credit line

❌ Ineffective Myths

Paying lump sum once

Closing all loans

Switching lenders frequently

🔹 Pros & Cons of Slow Credit Recovery

✅ Pros

Encourages genuine discipline

Prevents misuse of credit system

Rewards long-term responsibility

❌ Cons

Tests borrower patience

Delays access to low-cost loans

🔹 Key Takeaways

Credit reports reflect long-term behaviour

Negative entries fade slowly, not instantly

Recent discipline matters most

Consistency is the only real solution

🔹 Frequently Asked Questions (FAQs)

1. Why doesn’t my credit score improve immediately?

Because credit systems track behaviour over time.

2. How long does credit recovery take?

Anywhere from 6 months to 3 years.

3. Does closing loans improve credit faster?

No, it can sometimes hurt.

4. Can old mistakes be removed early?

Only if incorrectly reported.

5. Do recent EMIs matter more?

Yes, heavily.

6. Does income speed up recovery?

No, behaviour matters more.

7. Can I rebuild credit without loans?

Partially, but active credit helps.

8. Do multiple enquiries slow recovery?

Yes.

9. Is credit repair service useful?

Only for dispute resolution—not shortcuts.

10. Will score auto-improve with time?

Only if behaviour improves too.

11. Does RBI allow quick fixes?

No, to ensure system stability.

12. Is slow recovery a bad thing?

No—it ensures fairness and trust.

🔹 Conclusion + CTA

Credit reports aren’t designed for speed—they’re designed for trust. While improvement takes time, consistent discipline always works. The earlier you start good habits, the sooner lenders regain confidence in you.

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process. Apply at www.vizzve.com.

Published on : 7th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed