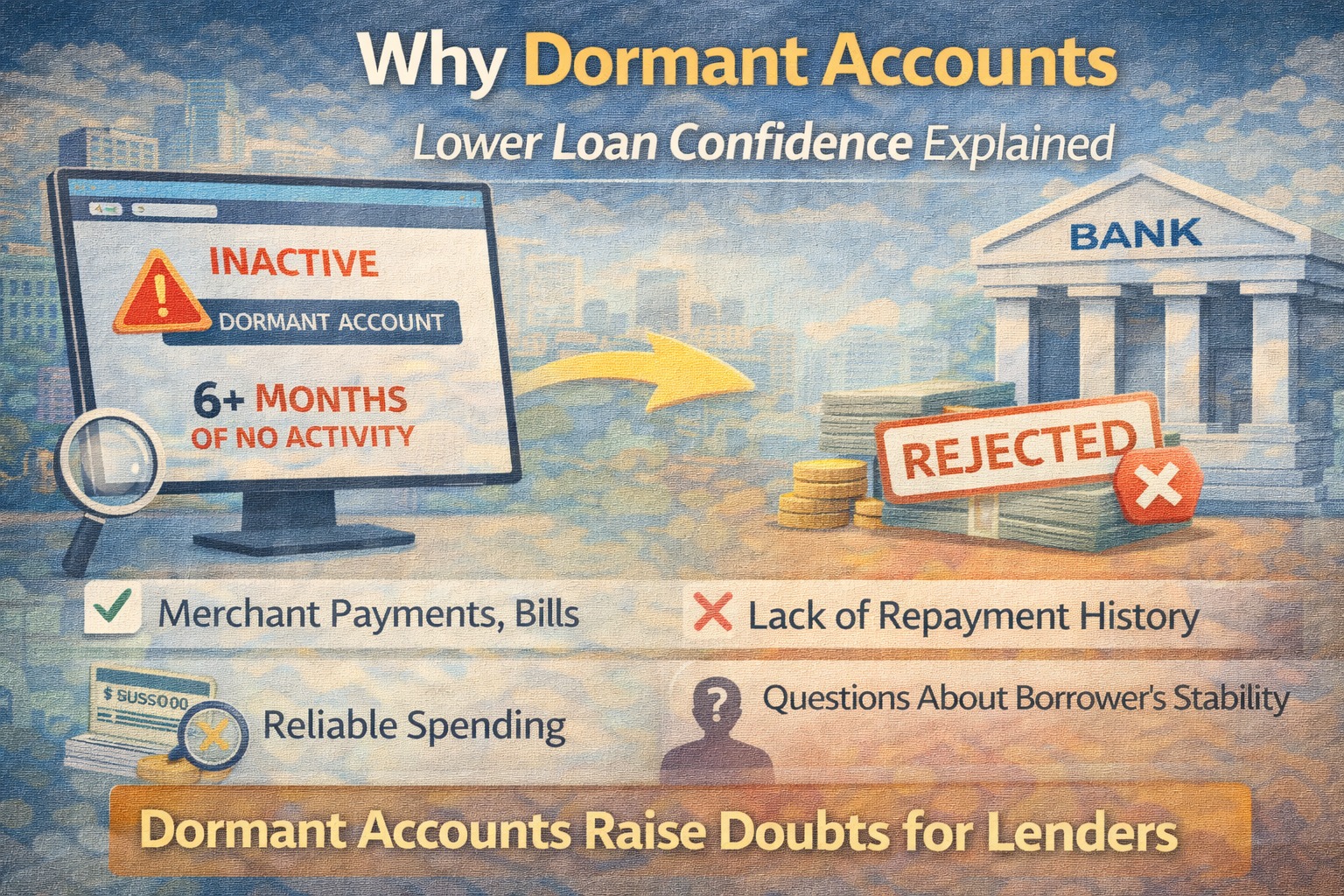

Dormant bank accounts reduce loan confidence because they signal inactive money management, unclear cash flow, and weak financial engagement—raising repayment risk in the eyes of lenders.

AI Answer Box (For Google AI Overview & AI Search)

Dormant accounts indicate financial inactivity and lack of transaction history. Lenders rely on active cash-flow patterns to assess repayment ability, so inactive accounts weaken credit confidence even if income and credit score look acceptable.

What Is a Dormant Account?

A bank account is considered dormant when:

No transactions occur for 6–12 months (varies by bank)

No salary credit, transfers, or spending

Account shows zero or static balance

Dormant doesn’t mean closed—but it does mean inactive.

Why Lenders Care About Account Activity

Banks don’t just check balances—they check behavior.

An active account shows:

Regular income flow

Spending discipline

EMI affordability

Financial engagement

A dormant account shows nothing—and uncertainty equals risk.

Key Reasons Dormant Accounts Lower Loan Confidence

1️⃣ No Cash-Flow Visibility

Without transactions, lenders can’t assess:

Monthly income stability

Expense patterns

EMI sustainability

No data = no confidence.

2️⃣ Signals Financial Inactivity

Dormant accounts suggest:

Salary shifted elsewhere

Business slowdown

Temporary or unstable income

This raises repayment doubts.

3️⃣ Breaks Financial Continuity

Lenders prefer:

Continuous financial trail

Predictable patterns

Dormancy creates gaps, which weaken underwriting comfort.

4️⃣ Raises Questions About Intent

Banks may ask:

Why was this account opened?

Why is it unused?

Is income being hidden or fragmented?

Too many unanswered questions reduce approval odds.

5️⃣ Hurts First-Time & Digital Borrowers More

For borrowers with:

No EMI history

Thin credit files

Dormant accounts remove an important alternate data signal.

Active vs Dormant Account (Lender View)

| Parameter | Active Account | Dormant Account |

|---|---|---|

| Income visibility | Clear | None |

| Spending pattern | Trackable | Missing |

| Cash-flow stability | Assessable | Unclear |

| Risk perception | Lower | Higher |

| Loan confidence | Strong | Weak |

Common Scenarios That Trigger Red Flags

Salary credited to a different account

Old accounts left unused

Business account inactive for months

Multiple zero-transaction accounts

One dormant account may not reject a loan—but multiple dormant accounts raise risk.

Expert Insight

“Lenders trust movement, not money sitting idle. An inactive account creates uncertainty, and uncertainty is priced as risk.”

— Retail Credit & Underwriting Expert

How to Fix Dormant Account Issues Before Applying

✅ 1. Reactivate the Account

Start regular transactions

Route salary or income temporarily

Use it for bills or EMIs

✅ 2. Show Consistency for 3–6 Months

Banks usually review:

Last 6 months of activity

Consistency matters more than amount.

✅ 3. Close Unnecessary Accounts

If you don’t need it:

Close it formally

Reduce clutter in financial profile

✅ 4. Consolidate Financial Activity

Fewer, active accounts are better than many inactive ones.

Myths (Busted)

❌ “Dormant accounts don’t matter”

✅ They affect cash-flow analysis

❌ “Only credit score matters”

✅ Behavior data matters too

❌ “Zero balance looks safe”

✅ Zero activity looks risky

Key Takeaways

Dormant accounts reduce lender confidence

No transactions = no cash-flow proof

Active accounts signal financial discipline

Fixing dormancy takes 3–6 months

Clean banking behavior improves approval odds

Conclusion

Dormant accounts don’t scream risk—but they whisper uncertainty, and lenders listen closely. In a cautious credit environment, banks prefer borrowers with visible, consistent financial behavior. Keeping your accounts active, consolidated, and disciplined is a simple but powerful way to boost loan confidence.

❓ Frequently Asked Questions (FAQs)

1. What is a dormant bank account?

A dormant bank account is one with no transactions for 6–12 months, depending on the bank’s policy.

2. Why do banks view dormant accounts negatively?

Because dormant accounts show no active cash flow, making it hard for lenders to assess repayment ability.

3. Can a single dormant account cause loan rejection?

Usually no, but multiple dormant accounts can significantly lower loan confidence.

4. Do digital lenders also check for dormant accounts?

Yes. Digital lenders use automated bank-statement analysis that flags inactive accounts.

5. How long does it take to fix a dormant account?

Typically 3–6 months of consistent activity makes an account look healthy again.

6. Should I close unused bank accounts?

Yes, if you don’t plan to use them. Fewer active accounts are better than many inactive ones.

7. Does a zero balance count as dormancy?

Zero balance alone doesn’t, but zero balance with no transactions does.

8. Can reactivating an account improve loan approval chances?

Yes. Regular transactions rebuild cash-flow visibility and trust.

9. Do dormant accounts affect credit score directly?

No, but they indirectly affect loan approval by weakening cash-flow analysis.

10. Are business dormant accounts riskier than personal ones?

Yes. Inactive business accounts raise serious income stability concerns.

11. How many months of bank statements do lenders review?

Usually 6 months, sometimes up to 12 months.

12. Does salary credited elsewhere create dormancy issues?

Yes. If salary is not credited to the account you submit, it may appear dormant.

13. Can savings-only accounts look dormant?

Yes, if there are no deposits or withdrawals for months.

Published on : 16th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed