In today’s lending environment, good credit behaviour matters more than income because lenders prioritize repayment discipline, credit history, and risk control over just how much you earn.

AI Answer Box

Why credit behaviour matters more than income:

Shows repayment reliability

Reduces lender risk

Improves loan approval chances

Lowers interest rates

Protects long-term financial access

Introduction

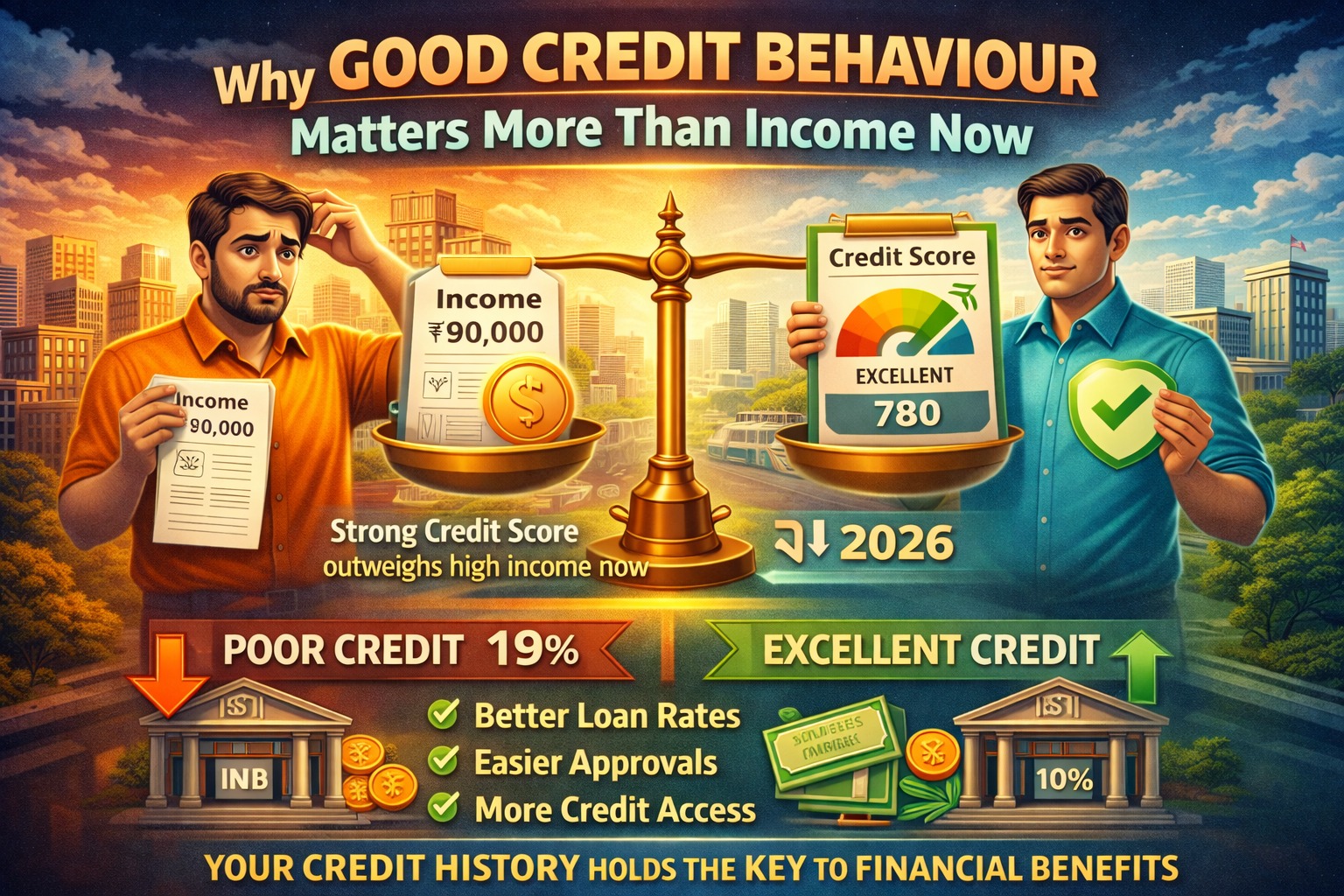

There was a time when a high salary almost guaranteed easy loan approval. That reality has changed. In 2026, lenders are far more cautious, data-driven, and focused on how you handle credit—not just how much you earn.

A borrower earning ₹40,000 with perfect credit behaviour can often get better loan terms than someone earning ₹1 lakh with poor repayment habits. Here’s why this shift is happening—and what it means for you.

What Is Credit Behaviour?

Credit behaviour refers to how responsibly you use and repay borrowed money over time.

Key Elements of Credit Behaviour:

Timely EMI and credit card payments

Credit utilization ratio

Number of active loans

Frequency of loan applications

Length and consistency of credit history

These factors together form your credit score and credit profile.

Why Income Alone Is No Longer Enough

1️⃣ Rising Loan Defaults

High-income borrowers are defaulting too—often due to:

Lifestyle inflation

Multiple EMIs

Overuse of credit cards

Income does not guarantee repayment discipline.

2️⃣ Data-Driven Lending Models

Banks and NBFCs now rely on:

Credit bureau data

Repayment patterns

Behavioural scoring models

These tools predict future repayment ability better than salary slips.

3️⃣ Regulatory & Risk Focus

The Reserve Bank of India has consistently emphasized:

Responsible lending

Risk-based pricing

Borrower behaviour monitoring

This has pushed lenders to reward good credit behaviour over high income.

Credit Behaviour vs Income: Real Comparison

| Factor | High Income, Poor Credit | Moderate Income, Good Credit |

|---|---|---|

| Loan Approval | Difficult | Easier |

| Interest Rate | Higher | Lower |

| EMI Flexibility | Limited | Better |

| Trust Level | Low | High |

| Long-Term Access | Weak | Strong |

How Good Credit Behaviour Benefits You

✅ Faster Loan Approvals

Clean credit history speeds up underwriting.

✅ Lower Interest Rates

Better scores = lower risk = cheaper loans.

✅ Higher Loan Eligibility

Lenders are willing to extend more credit responsibly.

✅ Financial Resilience

Good behaviour protects you during income shocks.

Common Credit Behaviour Mistakes

Paying only minimum credit card dues

Missing EMIs by a few days

Applying for multiple loans at once

Maxing out credit limits

Ignoring small overdue amounts

These actions damage trust—even if income is high.

How to Build Strong Credit Behaviour (Step-by-Step)

Pay all EMIs and bills on time

Keep credit card usage below 30%

Avoid unnecessary loan applications

Close unused credit lines responsibly

Monitor your credit report regularly

Consistency matters more than perfection.

Real-World Credit Insight

From real loan assessment experience, lenders increasingly reject high-income applicants with unstable credit behaviour, while approving lower-income borrowers with clean repayment records. Credit behaviour reflects financial discipline, which is the strongest predictor of repayment success.

Pros & Cons of Behaviour-Based Lending

✅ Pros

Fairer loan access

Encourages discipline

Reduces debt stress

❌ Cons

Past mistakes take time to correct

Limited flexibility for new borrowers

Key Takeaways

Income shows capacity; behaviour shows reliability

Credit behaviour now drives loan decisions

Good habits beat high salary in lending

Discipline today protects future borrowing

Frequently Asked Questions (FAQs)

1. Does income still matter for loans?

Yes, but less than credit behaviour.

2. Can low-income borrowers get loans easily?

Yes, with strong credit behaviour.

3. What matters more: salary or credit score?

Credit score and repayment history.

4. Can one missed EMI hurt loan chances?

Yes, especially recent defaults.

5. Do lenders check spending behaviour?

Indirectly, through credit data.

6. Is credit behaviour more important for personal loans?

Yes, because they are unsecured.

7. How long does it take to improve credit behaviour?

3–12 months with discipline.

8. Does prepaying loans help credit score?

Yes, if done properly.

9. Are credit cards bad for behaviour?

No, misuse is the problem.

10. Can RBI rules affect this trend?

Yes, RBI encourages risk-based lending.

11. Do NBFCs value behaviour too?

Yes, increasingly.

12. Is credit behaviour important even without loans?

Yes, it builds future eligibility.

Conclusion + CTA

In today’s financial system, how you borrow matters more than how much you earn. Good credit behaviour reflects discipline, responsibility, and reliability—qualities lenders trust far more than income figures.

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process. Apply at www.vizzve.com.

Published on : 7th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed