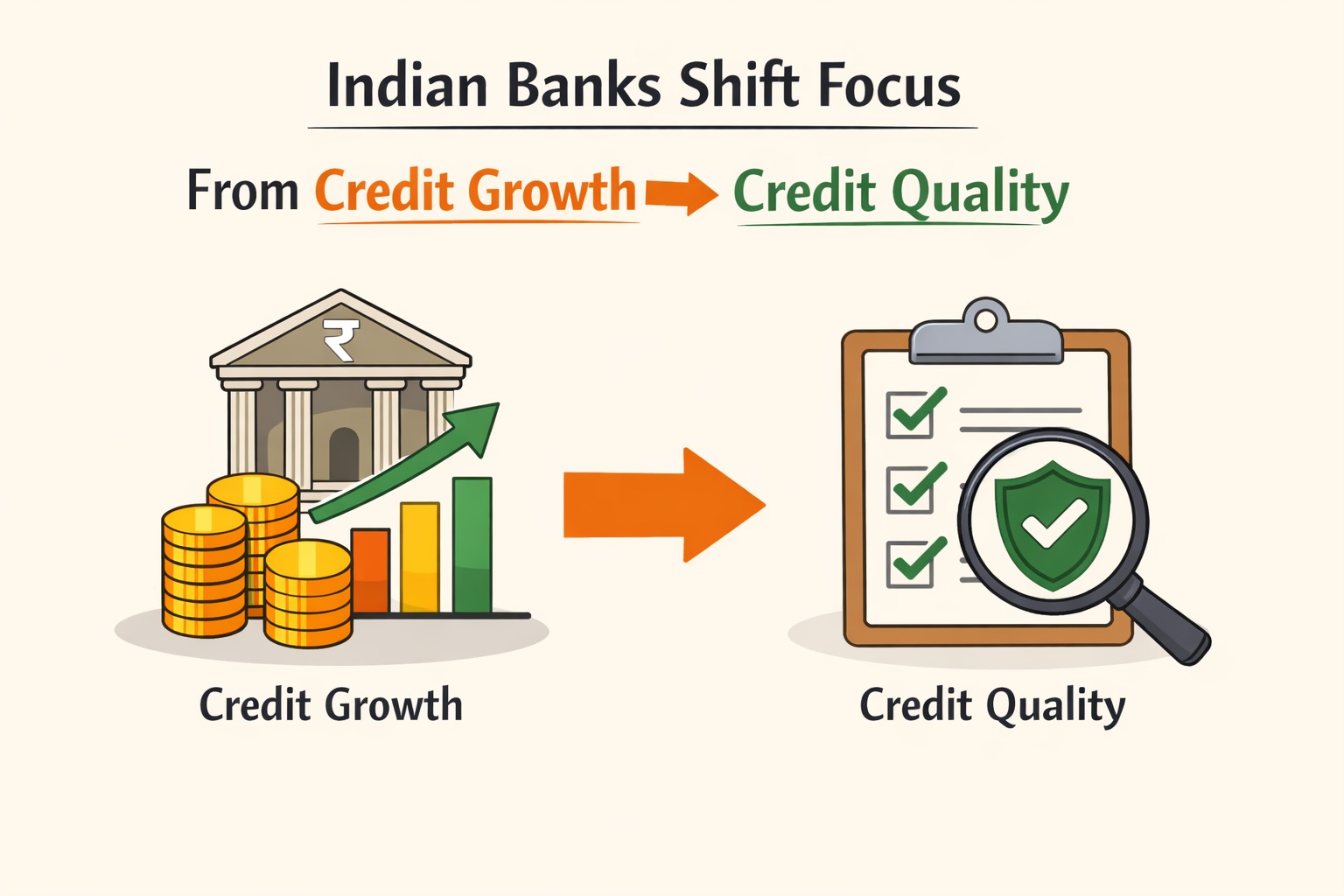

Indian banks are no longer chasing headline credit growth numbers.

Instead, they are quietly prioritising credit quality, borrower sustainability, and balance-sheet resilience.

This shift isn’t dramatic—but it’s structural. And it directly affects loan approvals, interest rates, and who gets funded in 2026.

AI Answer Box

Short Answer:

Indian banks are shifting from rapid credit growth to credit quality to avoid future NPAs, protect margins, and ensure long-term financial stability under tighter regulatory oversight.

What Is the Difference Between Credit Growth and Credit Quality?

Credit Growth

Focus on expanding loan books

Higher disbursals and volumes

Often prioritises speed and market share

Credit Quality

Focus on repayment sustainability

Risk-adjusted returns over volume

Emphasis on cash flow, affordability, and governance

📌 Banks are now choosing quality over quantity.

Why This Shift Is Happening Now

1. Lessons From Past NPA Cycles

Aggressive lending in earlier cycles led to:

Corporate loan stress

Rising NPAs

Capital erosion

Banks are determined not to repeat those mistakes.

2. Regulatory Focus on Early Risk Detection

Under guidance from the Reserve Bank of India, banks are:

Monitoring early stress signals

Tightening underwriting standards

Prioritising long-term repayment ability

📌 The goal: prevent stress, not manage defaults later.

3. Rising Household Leverage

Retail credit has grown rapidly, but banks now see:

Higher EMI burdens

Increased unsecured exposure

Stress signals before defaults

This is pushing lenders to slow down risky growth.

4. Margin Pressure and Cost of Capital

Low-quality growth:

Consumes more capital

Delivers weaker risk-adjusted returns

High-quality lending improves:

Net interest margins

Capital efficiency

Investor confidence

How Banks Are Implementing Credit Quality Focus

Practical Changes in Lending

Stricter EMI-to-income checks

Higher scrutiny of unsecured loans

Greater use of cash-flow analytics

Risk-based pricing replacing flat rates

Selective sector exposure

Retail vs Corporate Lending Under the Quality Lens

| Segment | Earlier Focus | 2026 Focus |

|---|---|---|

| Retail Loans | Rapid expansion | Affordability & EMI stress |

| Corporate Loans | Balance-sheet size | Project viability |

| MSME Loans | Volume-driven | Cash-flow clarity |

| Unsecured Credit | Growth-led | Risk-restricted |

What This Means for Borrowers

For Retail Borrowers

Credit scores alone aren’t enough

EMI burden and income stability matter more

Easy credit is disappearing

For Businesses

Governance and cash flow are critical

Informal practices face rejection

Disciplined MSMEs benefit

Expert Commentary

“Banks today would rather grow slowly than clean up bad loans later. Credit quality is now the growth strategy.”

From real-world portfolio reviews, even profitable borrowers are rejected if stress scenarios don’t hold up.

Is This Shift Good or Bad for the Economy?

✅ Positives

Stronger banking system

Lower systemic risk

Sustainable credit cycles

❌ Challenges

Slower credit access

Higher entry barriers

Pressure on marginal borrowers

How Borrowers Can Adapt to the New Reality

Step-by-Step

Keep EMI-to-income ratio below 35%

Maintain clean bank statements

Avoid stacking unsecured credit

Build repayment history before scaling

Focus on cash-flow visibility

Credit Growth vs Credit Quality: Snapshot

| Focus | Credit Growth Era | Credit Quality Era |

|---|---|---|

| Approval Speed | Fast | Deliberate |

| Pricing | Uniform | Risk-based |

| Risk Appetite | High | Disciplined |

| Borrower Type | Broad | Selective |

| Long-Term Stability | Weak | Strong |

Key Takeaways

Credit quality now drives lending decisions

Growth without sustainability is discouraged

RBI supervision reinforces discipline

Borrowers must show affordability, not optimism

This shift is structural, not temporary

Frequently Asked Questions

1. What is credit quality in banking?

It measures the likelihood of full and timely loan repayment.

2. Why are banks slowing credit growth?

To avoid future NPAs and protect capital.

3. Is RBI forcing banks to do this?

Indirectly, through risk and supervision norms.

4. Does this affect retail borrowers?

Yes, especially unsecured loan seekers.

5. Are corporate loans declining?

No, they are selective and quality-driven.

6. Is this trend permanent?

It’s a long-term structural shift.

7. Can good borrowers still get loans?

Yes, disciplined borrowers benefit.

8. Are NBFCs following the same trend?

Gradually, though at different speeds.

9. Will loan interest rates fall due to this?

Not necessarily; risk-based pricing dominates.

10. How can borrowers improve eligibility?

Reduce EMI burden and improve cash flow visibility.

11. Does credit score still matter?

Yes, but it’s no longer sufficient alone.

12. Is slower credit growth bad for GDP?

Short-term impact, long-term stability improves.

Conclusion: Quiet Discipline, Lasting Strength

Indian banks aren’t shouting about this change—but they’re executing it carefully.

The shift from credit growth to credit quality is shaping a safer, more resilient banking system, even if it feels restrictive to borrowers today.

CTA: Borrow Smarter in a Quality-First Era

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process. Apply at www.vizzve.com.

Published on : 21st January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed