Introduction

Every financial system runs on liquidity—the ability to access cash when needed.

Banks can be profitable, markets can be valuable, and borrowers can be creditworthy—but without liquidity, the system freezes. History shows that most financial crises begin not with losses, but with liquidity shortages.

This blog explains why liquidity is the backbone of any financial system, how it works, and why regulators guard it so closely.

AI Answer Box

Short Answer:

Liquidity is the backbone of a financial system because it ensures money can move smoothly between savers, banks, and borrowers. Without liquidity, even healthy institutions can fail.

What Is Liquidity in Simple Terms?

Liquidity means how easily assets can be converted into cash without losing value.

In the Financial System, Liquidity Means:

Banks can meet withdrawals

Loans can be disbursed on time

Markets can function without panic

Payments settle smoothly

📌 Liquidity is not about wealth—it’s about timing.

Why Liquidity Matters More Than Profitability

A bank can be:

Profitable

Well-capitalised

…and still collapse if it runs out of liquid funds.

📌 Profitability measures success over time.

📌 Liquidity measures survival today.

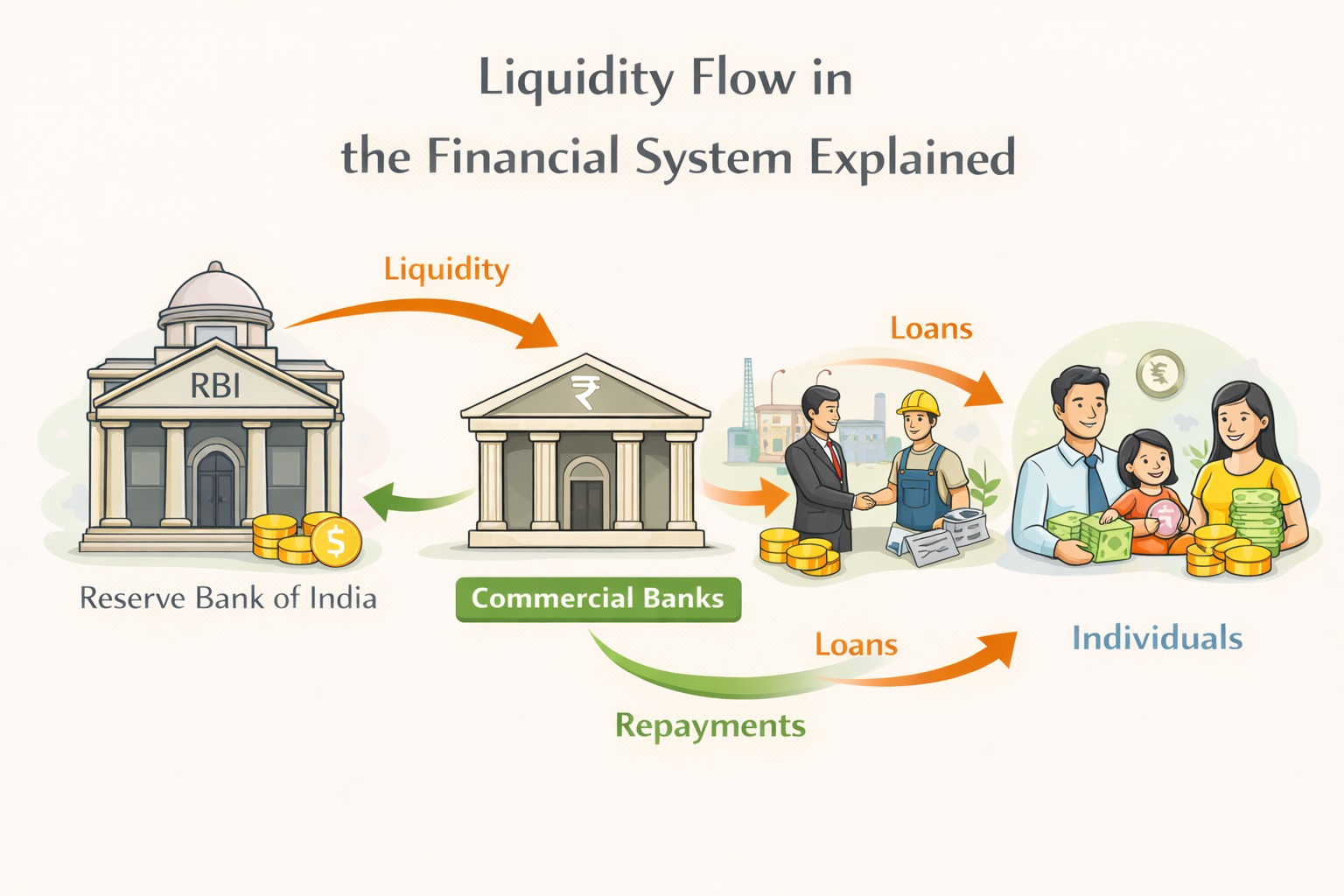

How Liquidity Flows Through the Financial System

Step-by-Step Liquidity Flow

Households deposit money into banks

Banks lend to individuals and businesses

Borrowers spend and invest, creating income

Money returns as deposits, taxes, or savings

Liquidity ensures this cycle never breaks.

Banks: The Heart of Liquidity Circulation

Banks perform three critical liquidity functions:

Transform short-term deposits into long-term loans

Manage daily cash needs

Provide confidence to depositors

Even a rumour-driven withdrawal can create liquidity stress.

Role of Central Banks in Liquidity Management

Central banks act as guardians of liquidity.

In India, the Reserve Bank of India:

Injects liquidity during stress

Absorbs excess liquidity during inflation

Acts as lender of last resort

Common Liquidity Tools

Repo & reverse repo

Open market operations

Standing facilities

Emergency funding windows

📌 These tools keep money flowing when markets hesitate.

Liquidity vs Solvency: A Critical Difference

| Aspect | Liquidity | Solvency |

|---|---|---|

| Meaning | Ability to pay now | Ability to pay eventually |

| Time Horizon | Short-term | Long-term |

| Crisis Trigger | Immediate | Gradual |

| Fix | Cash infusion | Capital infusion |

📌 Most crises start as liquidity problems, not solvency ones.

What Happens When Liquidity Dries Up

When liquidity tightens:

Banks stop lending

Markets freeze

Interest rates spike

Trust collapses

This leads to:

Credit crunch

Job losses

Economic slowdown

📌 Liquidity shocks spread faster than defaults.

Liquidity and Financial Crises (A Pattern)

Across global history:

2008 crisis

Pandemic-era stress

Banking scares

The common trigger was loss of liquidity confidence, not immediate losses.

Why Too Much Liquidity Is Also Risky

Excess liquidity can cause:

Asset bubbles

Excessive risk-taking

Inflation

That’s why regulators aim for balanced liquidity, not unlimited cash.

Liquidity in Modern Financial Systems

Today, liquidity flows through:

Banks and NBFCs

Money markets

Capital markets

Digital payment systems

Yet banks remain the core liquidity engines.

Real-World Insight

“A financial system doesn’t collapse when it runs out of money—it collapses when it runs out of trust and liquidity.”

From real banking stress scenarios, even strong institutions falter when short-term funding confidence disappears.

Why Liquidity Matters to Individuals

Liquidity affects you through:

Loan availability

Interest rates

Payment system stability

Access to savings

📌 When liquidity tightens, borrowers feel it first.

Key Takeaways

Liquidity keeps the financial system alive

Profit doesn’t replace cash access

Central banks manage liquidity actively

Liquidity shortages trigger crises

Balanced liquidity ensures stability

Frequently Asked Questions

1. What is liquidity in finance?

Ease of accessing cash when needed.

2. Why is liquidity important for banks?

To meet withdrawals and lending needs.

3. Can profitable banks fail due to liquidity?

Yes.

4. Who controls liquidity in India?

The Reserve Bank of India.

5. What causes liquidity crunch?

Panic, risk aversion, or policy tightening.

6. Is liquidity same as capital?

No, they serve different purposes.

7. How do central banks add liquidity?

Through repo and market operations.

8. Can too much liquidity be harmful?

Yes, it can fuel inflation and bubbles.

9. Does liquidity affect loan interest rates?

Directly.

10. Is liquidity important for markets?

Yes, it ensures smooth trading.

11. How does liquidity affect economic growth?

Adequate liquidity supports growth.

12. Why do regulators monitor liquidity closely?

To prevent systemic crises.

Conclusion: Liquidity Is the System’s Lifeline

Liquidity is the financial system’s oxygen.

When it flows, everything works quietly. When it stops, even strong institutions struggle.

That’s why central banks, regulators, and markets obsess over liquidity—because without it, nothing else matters.

CTA: Smarter Borrowing Support

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process. Apply at www.vizzve.com.

Published on : 24th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed