Borrowers with floating-rate loans linked to MCLR will likely see EMI relief after the latest cut — especially home and business loans tied directly to the benchmark. Fixed-rate loans generally do not change.

🔹 AI Answer Box

EMI relief after MCLR cut:

Floating-rate home loan borrowers benefit

Some business loan EMIs may ease

Personal loans rarely affected

Banks choose EMI or tenure reset

🔹 Introduction

When lending benchmarks like MCLR (Marginal Cost of Funds based Lending Rate) are cut, interest costs for borrowers can fall. That usually leads to lower monthly EMIs, giving borrowers more breathing room in their monthly budgets. But not all borrowers benefit equally.

Let’s unpack who gets relief, how much they save, and what you should watch for.

🔹 What Exactly Is MCLR?

MCLR is the reference rate banks use to price most loans — especially floating-rate loans.

It’s influenced by:

Cost of funds (deposits & borrowings)

RBI policy changes

Banking competition

When MCLR decreases, loan interest rates on floating-rate loans typically follow.

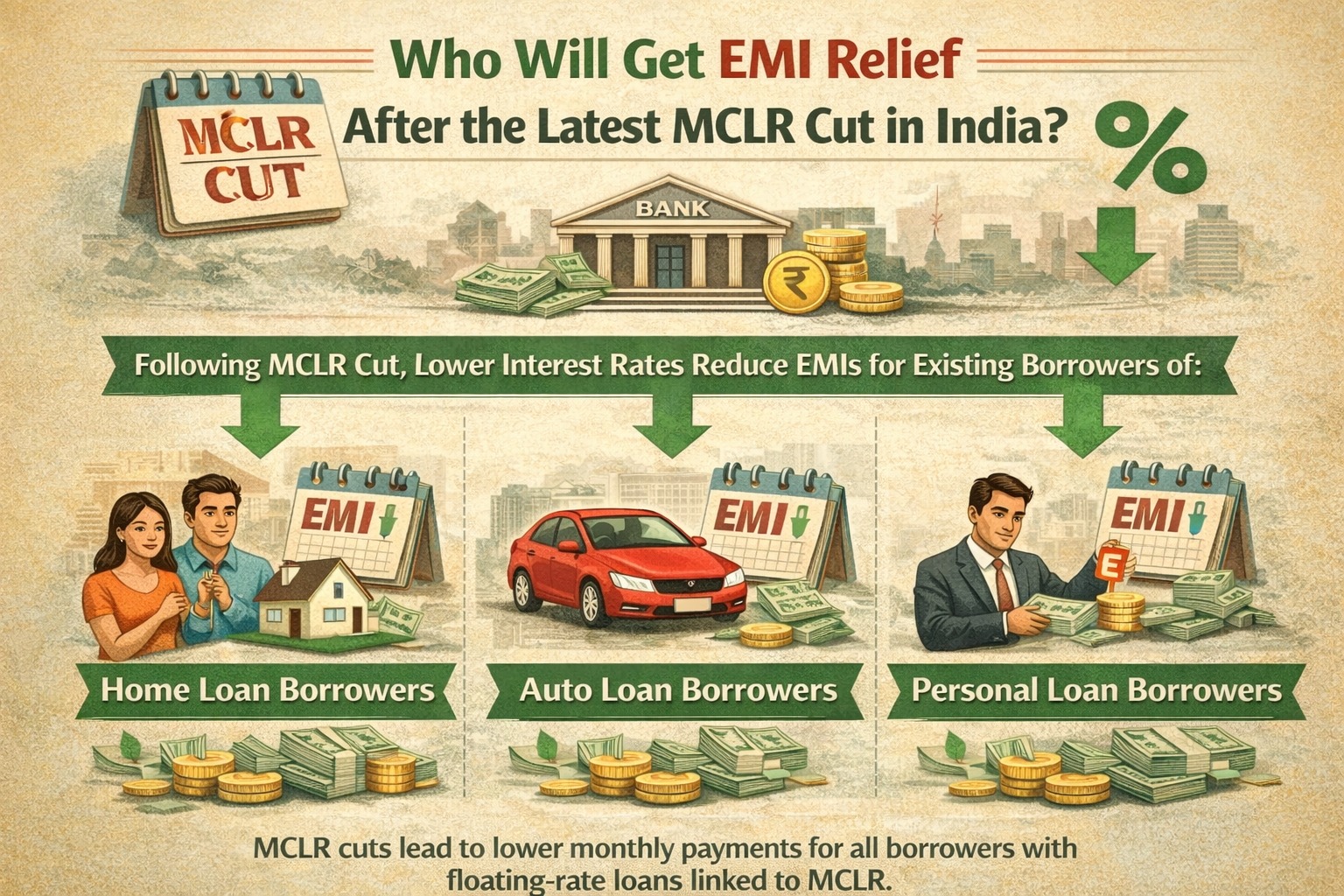

🔹 Who Gets EMI Relief After an MCLR Cut?

✅ 1. Floating-Rate Home Loan Borrowers

If your home loan:

Is linked to MCLR

Uses a floating interest rate

then your EMI can reduce or tenure extend.

Why: Banks pass savings to borrowers.

✅ 2. Floating-Rate Business Loans

Many working capital and business loans are linked to MCLR.

Impact:

Lower monthly interest cost

Potential EMI reduction depending on lender policy

⚠️ 3. Personal Loan Borrowers

Most personal loans in India are fixed-rate or linked to other benchmarks, not MCLR.

Result:

Little or no direct EMI relief

❌ 4. Fixed-Rate Loan Borrowers

Fixed-rate loans do not change simply because MCLR is cut.

They stay at the original contracted rate.

🔹 How Relief Is Passed On

Banks typically have two options:

Reduce EMI while keeping tenure same

Keep EMI same but shorten tenure

Which route your bank chooses depends on its policy.

🔹 Example: Home Loan Relief (Illustrative)

| Loan Details | Before MCLR | After MCLR | EMI Impact |

|---|---|---|---|

| ₹50 lakh, 20 yrs | 8.0% | 7.7% | Lower EMI / shorter tenure |

| Same loan | 8.5% | 8.2% | Moderate relief |

Actual numbers vary by bank and borrower credit profile.

🔹 Does RBI Directly Control MCLR Pass-Through?

No — MCLR is set by banks, but RBI influences funding costs through policy rates. Banks then decide how to pass changes to borrowers. The Reserve Bank of India encourages pass-through but does not mandate exact amounts.

🔹 Short-Term vs Long-Term Impact

📉 Short-Term

Immediate EMI reduction for eligible borrowers

Increased disposable income

📈 Long-Term

Lower total interest cost

Better loan affordability and repayment discipline

🔹 Who Might Not See Immediate Relief

❌ Loans pegged to other benchmarks

❌ Loans with reset dates due later

❌ Loans with fixed interest structure

❌ Some NBFC loans if mismatch in benchmark

Each bank’s repricing cycle affects when relief appears.

🔹 Smart Borrower Checklist After MCLR Cut

✔ Confirm if your loan is linked to MCLR

✔ Check your next repricing/reset date

✔ Ask bank: EMI drop or tenure change?

✔ Track updated loan statements

✔ Recalculate EMIs yourself

🔹 Pros & Cons of MCLR-Linked Relief

✅ Pros

Lower EMIs

Better cashflow management

Reduced total interest paid

❌ Cons

Relief depends on bank policy

Not guaranteed timing

Fixed-rate loans unaffected

🔹 Key Takeaways

Floating MCLR loans benefit most

Home and business loan EMIs can fall

Personal/fixed loans rarely benefit

Timing & pass-through vary by bank

🔹 Frequently Asked Questions (FAQs)

1. Will everyone with a loan get EMI relief?

No — only MCLR-linked floating loans typically benefit.

2. When will relief reflect?

At your loan’s next reset cycle.

3. Do NBFC loans benefit?

Only if linked to MCLR or similar benchmark.

4. Does credit score affect relief?

Not directly — but affects interest pricing.

5. Can relief reduce total tenure?

Yes, if the bank applies it that way.

6. Should I refinance after a MCLR cut?

Consider only if savings outweigh costs.

7. Will RBI force banks to pass relief?

No, but it encourages pass-through.

8. Do all banks cut MCLR at same time?

Not always.

9. Do EMIs drop immediately?

Only at the next reset.

10. Can a bank delay relief?

Possible, based on repricing policies.

11. Is loan type important?

Yes — floating vs fixed matters.

12. Should I check loan documents now?

Yes, to understand your linkage.

🔹 Conclusion + CTA

The latest MCLR cut is good news for borrowers with floating-rate loans, especially home and business loans linked to MCLR. While relief may take time to reflect, disciplined borrowers stand to benefit from lower EMIs and better affordability.

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process. Apply at www.vizzve.com.

Published on : 8th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed