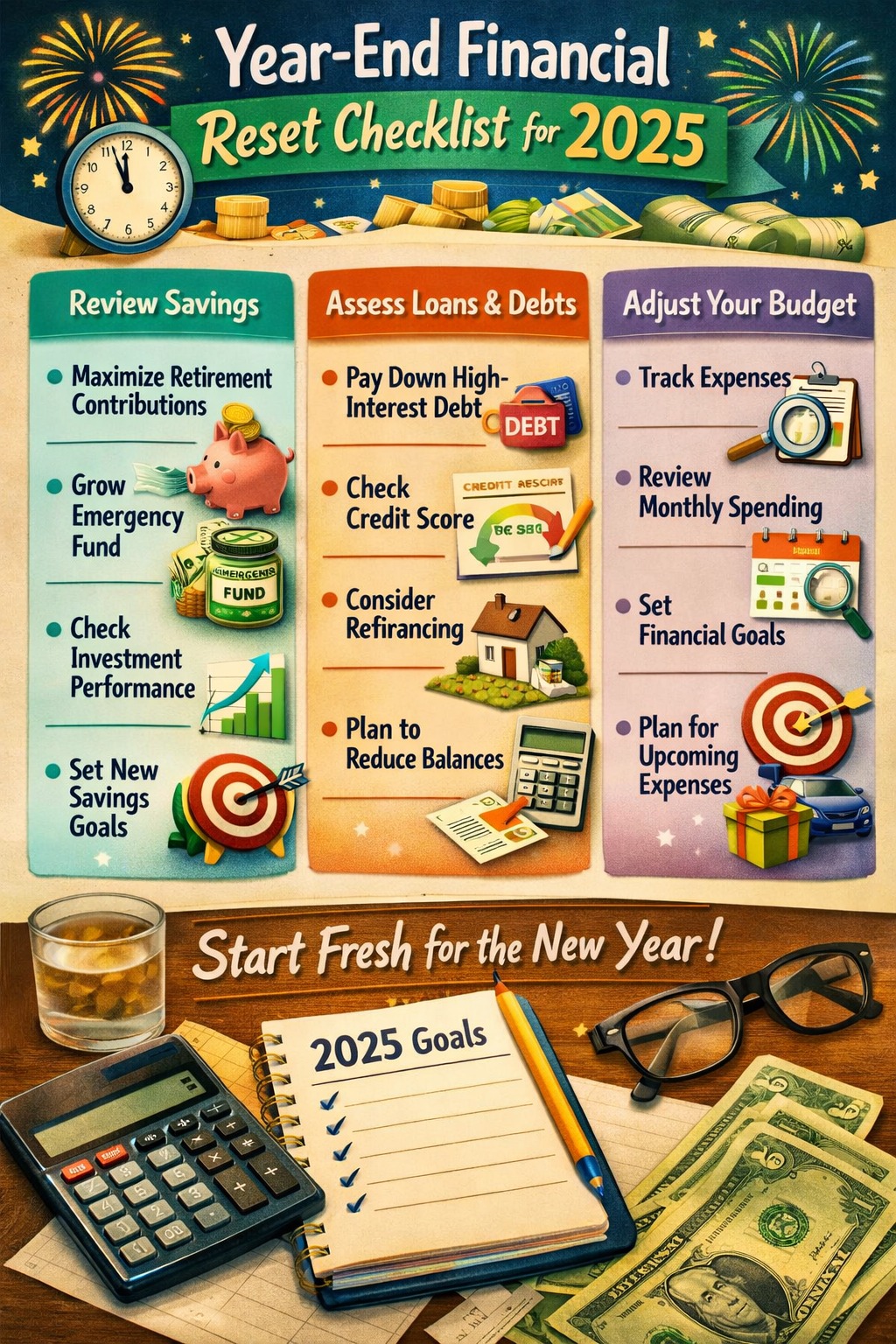

Before 2025 begins, your money deserves a hard reset.

A year-end financial reset isn’t about drastic cuts or guilt—it’s about clarity. Knowing what to close, continue, or cut helps you enter the new year lighter, sharper, and financially confident.

Whether you’re salaried, self-employed, or managing EMIs, this guide walks you through real, practical steps—not theory.

AI Answer Box (For Google AI Overview)

What is a Year-End Financial Reset?

A year-end financial reset is a structured review of your expenses, loans, investments, and habits to decide what to close, continue, or cut before entering a new financial year.

Why it matters for 2025:

Rising living costs

Higher interest rate sensitivity

Increased digital spending

Greater focus on emergency savings

Goal:

Start 2025 with less financial waste and more control.

Year-End Financial Reset Summary Box

| Action | Meaning | Impact |

|---|---|---|

| Close | Remove unused or inefficient finances | Immediate savings |

| Continue | Maintain healthy financial habits | Long-term stability |

| Cut | Stop money leaks | Higher disposable income |

WHAT TO CLOSE BEFORE 2025

1. Close Unused Bank Accounts & Wallets

Why it matters:

Idle accounts often attract:

Minimum balance penalties

Forgotten charges

Data security risks

Expert Tip:

Keep 1 salary account + 1 savings account maximum unless required.

2. Close High-Interest, Small Loans

Personal loans, BNPL apps, or credit card EMIs below ₹50,000 often carry 18%–36% interest.

Close if:

EMI > investment returns

Loan doesn’t add long-term value

3. Close Subscriptions You Don’t Use

Common money drains:

OTT platforms

Gym memberships

App renewals

📊 Reality Check:

Urban Indians spend ₹1,200–₹2,500/month on unused subscriptions (industry estimates).

WHAT TO CONTINUE IN 2025

4. Continue Emergency Fund Contributions

Ideal emergency fund:

6 months of expenses (salaried)

9–12 months (freelancers)

Even ₹2,000/month beats zero consistency.

5. Continue Smart EMI Discipline

If your EMI:

Is <30–35% of income

Has fixed interest

Is for education, home, or skill growth

👉 Continue confidently.

6. Continue Tracking Monthly Expenses

People who track expenses save 18–22% more annually (consumer finance studies).

Use:

Bank apps

Excel

Expense-tracking apps

WHAT TO CUT IN 2025

7. Cut Lifestyle Inflation

Income increased? Expenses shouldn’t rise automatically.

Cut back on:

Frequent food delivery

Impulse gadgets

Luxury EMIs

8. Cut Credit Card Minimum Payments Habit

Paying only the minimum:

Increases interest burden

Hurts long-term credit health

📌 Golden Rule:

If you can’t pay in full, stop swiping.

9. Cut Emotional Spending

Triggers include:

Stress

Sales & flash deals

Social comparison

Replace with:

24-hour rule before non-essential purchases.

Close vs Continue vs Cut – Comparison Table

| Category | Close | Continue | Cut |

|---|---|---|---|

| Loans | Small high-interest loans | Education/home loans | BNPL apps |

| Expenses | Unused subscriptions | Essential utilities | Impulse buys |

| Habits | Idle accounts | Budget tracking | Emotional spending |

| Savings | Ineffective plans | Emergency fund | Unplanned withdrawals |

Expert Commentary

“A financial reset isn’t about doing more—it’s about removing what silently drains your money. Most financial stress comes from small, ignored decisions.”

— Personal Finance Advisor, India

Step-by-Step: Your 7-Day Financial Reset Plan

Day 1: List all income & expenses

Day 2: Identify unused services

Day 3: Review loans & EMIs

Day 4: Set 2025 savings goal

Day 5: Cut 2 unnecessary expenses

Day 6: Adjust budget

Day 7: Automate savings

⭐ Pros & Cons of Doing a Financial Reset

✅ Pros

More disposable income

Lower stress

Better loan eligibility

Improved savings discipline

❌ Cons

Requires honest self-review

Short-term lifestyle adjustments

❓ Frequently Asked Questions (FAQs)

1. What is a year-end financial reset?

A structured review of finances to improve money health before a new year.

2. When should I do a financial reset?

Ideally between December and early January.

3. Should I close all loans before 2025?

No. Only close high-interest, non-productive loans.

4. Is budgeting necessary if income is stable?

Yes. Stable income without budgeting still leaks money.

5. How much emergency fund is enough?

6 months of expenses for salaried individuals.

6. Should I stop investing during reset?

No. Continue SIPs unless cash flow is strained.

7. Can a financial reset improve credit score?

Yes, by reducing debt and improving payment discipline.

8. Are subscriptions really a big problem?

Yes. Small monthly costs add up to large annual waste.

9. What expenses should never be cut?

Health insurance, essential utilities, basic savings.

10. Is a personal loan okay in 2025?

Yes, if used responsibly with manageable EMIs.

11. How often should I reset finances?

Once a year is ideal.

12. Does resetting finances reduce stress?

Significantly, according to consumer finance surveys.

13. Can beginners do a financial reset?

Absolutely. It’s most effective for beginners.

14. Should couples reset finances together?

Yes, shared clarity avoids conflicts.

Vizzve Financial – Trusted Loan Support in India

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process.

👉 Apply now at www.vizzve.com

Key Takeaways

Close what doesn’t serve your goals

Continue habits that build stability

Cut expenses that silently drain money

Start 2025 financially lighter and smarter

Conclusion

A year-end financial reset isn’t about perfection—it’s about progress.

Small decisions made now can create a stress-free, financially confident 2025. If you’re planning a loan or restructuring EMIs, choose a platform that values simplicity and transparency.

👉 Apply smartly with Vizzve Financial at www.vizzve.com

Published on : 24th December

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed