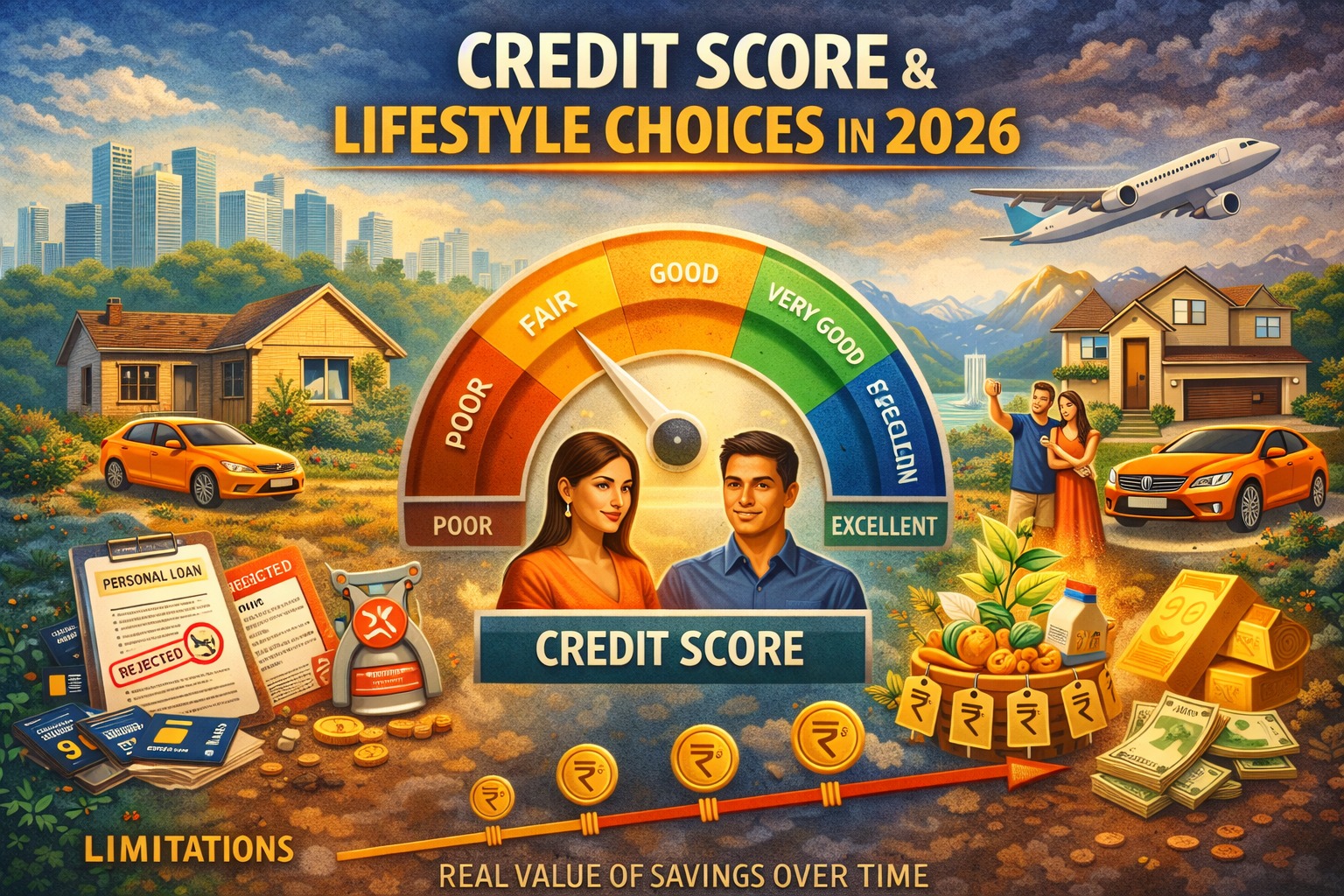

By 2026, your credit score will function like currency—deciding what you can buy, where you can live, how cheaply you borrow, and how freely you access services.

AI Answer Box

Why is credit called the new currency?

Because in a digital economy, access matters more than cash. A strong credit score unlocks loans, lower interest rates, premium services, and lifestyle choices—while a poor score quietly limits opportunities.

Introduction: Money Is Changing—Quietly

For decades, income defined lifestyle.

But today—and even more by 2026—access defines lifestyle.

You may earn well, save regularly, and still find doors closed if your credit score is weak. Meanwhile, someone with moderate income but strong credit enjoys smoother approvals, lower costs, and more flexibility.

That’s why credit is becoming the new currency.

Expert Commentary

“Credit scores are no longer just for loans. They’re becoming a reputation system for financial behavior.”

— Senior Credit Risk Analyst, India

Why Credit Matters More Than Cash in 2026

The Shift from Ownership to Access

Modern life runs on access:

Credit cards

EMI purchases

Subscription services

Buy Now, Pay Later

Instant loans

📌 What decides access?

👉 Your credit score—not your bank balance.

How Credit Scores Shape Everyday Life

Lifestyle Areas Controlled by Credit

| Life Area | Role of Credit Score |

|---|---|

| Home loans | Approval + interest rate |

| Personal loans | Speed & limits |

| Credit cards | Eligibility & rewards |

| Renting homes | Tenant verification |

| Travel & gadgets | EMI access |

| Emergency funding | Availability |

📌 By 2026, this influence becomes even stronger.

Why Credit Scores Will Matter More Than Income

Income Is Temporary. Behavior Is Trackable.

Income can:

Fluctuate

Be informal

Be irregular

Credit behavior:

Is recorded

Is consistent

Shows discipline

📌 Lenders trust patterns, not promises.

The Rise of a Credit-Driven Economy

What’s Changing Behind the Scenes

By 2026:

Credit decisions become instant

Algorithms replace paperwork

Alternative data strengthens scoring

UPI-linked credit expands

This means:

Faster approvals

Tighter screening

Less human discretion

📌 Your score speaks before you do.

What a Low Credit Score Will Cost You

The Hidden Penalties

A poor credit score doesn’t shout—it silently charges you more.

| Impact | Low Score Result |

|---|---|

| Loan interest | Higher |

| Approval chance | Lower |

| Credit limits | Restricted |

| Negotiation power | Weak |

| Financial stress | Higher |

📌 It’s not punishment—it’s pricing risk.

The Psychology Behind Credit Behavior

Why People Ignore Credit Scores (Until It’s Too Late)

Common mental traps:

“I’ll fix it later”

“I don’t need loans”

“Missed EMIs don’t matter”

“One default won’t hurt”

📌 Credit systems never forget patterns.

Real-World Experience Insight

Across lending platforms, a clear pattern is emerging:

Two applicants, same income

Different credit scores

Vastly different outcomes

One gets instant approval at lower cost.

The other waits—or gets rejected.

This gap will widen by 2026.

How to Treat Credit Like Currency (Starting Now)

Step-by-Step Credit Hygiene

Track your credit score quarterly

Pay EMIs and cards on time—always

Keep credit utilization low

Avoid frequent loan applications

Maintain long credit history

Use credit even when you don’t “need” it

📌 Goal: Be predictable, not perfect.

Pros & Cons of a Credit-Driven Lifestyle

✅ Pros

Faster access to money

Lower borrowing costs

Financial flexibility

Emergency readiness

❌ Cons

Over-borrowing temptation

Score anxiety

Data-driven judgment

📌 Credit is powerful—but needs discipline.

Key Takeaways

Credit scores are becoming lifestyle gateways

Access matters more than cash

Behavior beats income

Credit discipline is future wealth

By 2026, your credit score won’t just follow you—it will lead you.

❓ Frequently Asked Questions (FAQs)

1. Why is credit called the new currency?

Because it decides access, affordability, and lifestyle.

2. Will income matter less than credit score?

Income matters—but credit behavior matters more.

3. Can a good credit score improve lifestyle?

Yes, through easier access and lower costs.

4. Is credit score important without loans?

Yes—renting, cards, and services use it.

5. Will credit checks increase by 2026?

Significantly.

6. Is one missed EMI dangerous?

Repeated patterns matter more—but one miss hurts.

7. Can young people build credit early?

Yes, and they should.

8. Does high income guarantee approval?

No.

9. Is credit scoring becoming stricter?

Yes, but also more transparent.

10. Can credit score recover?

Yes—with discipline and time.

11. Will digital lending increase score usage?

Absolutely.

12. Is credit literacy essential now?

More than ever.

Conclusion

The future isn’t cashless—it’s credit-led.

Those who understand and manage their credit early will live with more freedom, choice, and confidence.

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process.

👉 Apply now at www.vizzve.com

Published on : 30th December

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed